A New Theory of Monetary Long Cycles under Scrutiny of First Round Empirical Tests

скачать скачать Автор: Jourdon, P. - подписаться на статьи автора

Журнал: Journal of Globalization Studies. Volume 2, Number 2 / November 2011 - подписаться на статьи журнала

In the present article the author reconsiders the theories of long monetary cycles by Marjolin (1941) and Dupriez (1966) in order to update their practical application to the 21st century. This leads to the recommendation to rely on the euro for a social project – consisting of balancing protection of private, social and self-property – and to monitor simultaneously three parameters: external (geopolitical), internal (social), and contingent (economic). This new method is designed with a view to contribute to the future balance in world affairs.

Keywords: monetary cycles, Kondratieff cycles, economic crisis, world governance.

Introduction

In our previous paper A New Theory of Monetary Long Cycles, with Assumptions Fitted to the Twenty-first Century (Jourdon 2011), we showed that the theories of monetary long cycles produced by Marjolin (1941) and Dupriez (1966) could present their results supplemented by the introduction of new hypotheses and data, more fitting the 21st century (financial innovations, global development). Their common framework can be useful if we come to the conclusion of the world system's deadlock today: for the first time in history the major international financial crisis could only be solved through the resolution of a world scale tax issue. This shows the failure of purely national attempts to cope with the crisis. The growing indebtedness has called for individualistic, legal, solutions in order to declare companies' and households' earnings and pay less tax – relevant from the sole micro economic standpoint of private investments. It does help private interests to consider more rationally their patrimony or projects, but the massive macro-economic side effect brings no answer to state indebtedness, a dangerous confusion in the balance of payments, and even in the balance sheets of financial institutions. If we take this probable assumption of an unedited world scale tax problem as the starting point of our synthesis, we may suggest a new geometry for future economy modelling. There will be a contingent (economic) parameter, resulting from frictions between external (geopolitical) and internal (social) parameters. Starting from these settings, a new perspective would ask the euro to be the vehicle useful for a worldwide planned convergence. In this paper, we investigate the empirical tests of our theory of long monetary cycles, showing the whole integrating picture from £ Sterling (1848–1945), passing through US $ (1917–2015), and then coming to the perspectives for euro (1992–2090). It seems well fitting a statistical regression pattern and a clear evolutionary path associating a new social project with each successive key currency.

Results Presentation

1848–1945: £ Sterling

Monetary mass + savings related to the £ Sterling: increased by 50 % between 1848 and 1860 (Appendix).1

It is the formation of the mechanisms of ‘financial reserves’ and legal reserves related to the key currency. It became the key currency in the 1870s, when the gold standard regime began. From 1870 to 1914 the trade balance and current account balance of theUnited Kingdom (UK) were consistently producing strong surplus, and the key currency became increasingly influential (Aglietta 1979). Besides, the rising debt did not apply directly to the United Kingdom but to the countries linked to the key currency. The countries in the first periphery (France, Germany…) took an opportunity to increase their monetary mass, thinking that the UK would assume responsibility. The European periphery countries became heavily indebted towards the UK and countries of the first periphery. Throughout this period, the UK fixed interest rates. The waning period of the pound (1917–1945), with the dollar coming afterwards, is well known: the phenomenon of indebtedness of countries in the European periphery is proven (Flandreau and Le Cacheux 1997). From 1873 to 1896, the debt rose in many countries to over 80 per cent of national GDP, sometimes rose even above 100 per cent of GDP (Table 1). In 1880–1896 the United Kingdom's public debt remained rather constant (about 50 per cent of GDP). In Belgium, Holland and France, the average figures were about 80 per cent. In Sweden, Norway and Denmark, they fluctuated on average around 55 per cent. In Spain, Portugal and Greece, the figures around 90 per cent were observed.

Table 1

Public debt in the European system: 1880–1896

|

|

United Kingdom |

Belgium, Holland, France: Average |

Sweden, Norway, Denmark: Average |

Spain, Portugal, Greece: Average |

|

1880–1882 |

59 |

– |

– |

90.1 |

|

1883–1885 |

50.3 |

77.7 |

47.7 |

83.5 |

|

1886–1888 |

48.3 |

85.6 |

54.5 |

86 |

|

1889–1891 |

47 |

79.8 |

53.3 |

93.7 |

|

1892–1894 |

46 |

82.5 |

55.3 |

100 |

|

1895–1896 |

42 |

83.7 |

52.6 |

99.7 |

|

Average |

49.2 |

~~ 81.8 |

~~ 53.4 |

~~ 90.5 |

Source: figures showed in the graph 1 ‘Ratio dette / PIB en Europe. 1880–1914’ in Flandreau and Le Cacheux 1997: 532.

From 1896 all public debts began to decrease (Table 2). National debts which used to fluctuate above 100 per cent fell below. Public debts of countries figured above 80 per cent fell down to 60 per cent. The UK debt was below 60 per cent (from 1897 to 1914 British figures amounted on average to about 40 %), and the first circle stood above 80 per cent most of the time (70 per cent on average for Belgium, Holland and France). Only ‘neutral’ countries (in Scandinavian region, Switzerland), managed to avoid the over-indebtedness and hovered at around 35 per cent. In Spain, Portugal and Greece, figures reached as much as an average of 95 per cent.

Table 2

Public debt in the European system: 1897–1913

|

|

United Kingdom |

Belgium, Holland, France: Average |

Sweden, Norway, Denmark, Switzerland: Average |

Spain, Portugal, Greece: Average |

|

1897–1899 |

39.7 |

77.3 |

– |

100.8 |

|

1900–1902 |

40 |

75.9 |

38 |

107.2 |

|

1903–1905 |

40 |

72 |

35.9 |

97.7 |

|

1906–1908 |

38 |

65.6 |

32.75 |

93.9 |

|

1909–1911 |

36 |

65.2 |

32.9 |

89.1 |

|

1912–1913 |

33.5 |

55.5 |

– |

83.7 |

|

Average |

37.8 |

~~ 69.1 |

~~ 35.1 |

~~ 96.5 |

Source: figures showed in the graph 1 ‘Ratio dette / PIB en Europe. 1880–1914’ in Flandreau and Le Cacheux 1997: 532.

The Mediterranean countries were close to 100 per cent of debt compared with the national GDPs, and the debt was never below 80 per cent. Besides, from 1895 the countries most affected by debt found lower debt rates (than 80 per cent)… but it was too late to prevent the march to war, as these countries witnessed social movement and riots throughout the preceding twenty years.

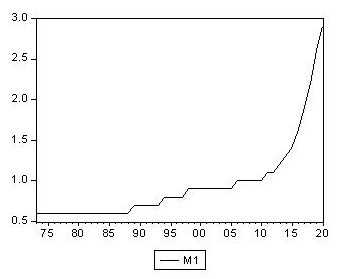

Diagram 1. The consideration of the monetary long cycle of the £ Sterling (1848–1945),

M1 in £ Sterling, from 1873 to 1920

Source: Graph in Jourdon 2010b: 1794. Figures used: ‘Money Stock’ (million £), in Friedman and Schwartz 1982: 130–132.

Commentaries:

– The econometric analysis shows that an exponential explanation is quite good. A logistic explanation fits as well. We can note that since the logistic explanation fits quite well, the theory of the monetary long cycle – with S-curve – could be applied (Jourdon 2010a: 1089–1090, 1136–1138). This is the cyclical explanation. But the cycle is within the tendency which stands for the worldwide monetarization. This explains the preparative ‘exponential’ third period of the cycle.

- Here the second period of the cycle is shown (the increase in influence and indebtedness) (Jourdon 2010a: 1095–1097). A display of the first period (1848–1973) would show a stable preparation of financial reserves. The third period (1917–1945) would be much more complex because it shows the consequences – emulation and perturbation – of the growing competition with the US dollar in search for a wider influence (Jourdon 2010a: 1140–1142, 1146–1147).

- The display of the evolution of £ Sterling and its natural monetary ally at that time (the French Franc) would still amplify the results shown here in the Diagram.

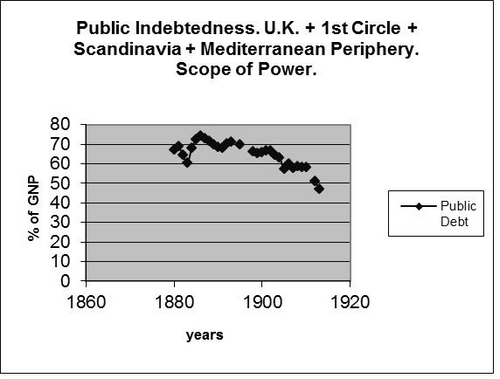

Diagram 2. The consideration of the monetary long cycle of the £ Sterling (1848–1945), f growing indebtedness during the second period of the cycle (1873–1917):

Source: Jourdon 2010b: 1789. Figures by Jourdon 2010b: 1706–12.

Commentaries:

- The curve shows a smooth increase in the indebtedness of the European monetary complex (United Kingdom + 1st Circle France, Holland, Belgium + ‘neutral countries’ Denmark, Norway, Sweden, Switzerland + Mediterranean countries: Greece, Portugal, Spain) up to 1886 (77 per cent of public debt compared with national GDP), and then the following long decrease up to 56 per cent in 1913. This came too late to avoid upheavals. Then a ‘shots bar’. We failed to get any consolidated figures with respect to Germany.

- This presentation of indebtedness rates in the second period of the cycle seems to corroborate our assumptions about the inner dynamics of the cycle (with indebtedness in its second period). It has to be completed with strategic examination of the behaviour of the system core (the United Kingdom + 1st Circle) compared with the periphery. Such an examination shows that the UK tolerated the other countries becoming slightly more indebted than the UK itself was. It also shows that, for the Mediterranean countries, the indebtedness was much more than 100 per cent in 1880 (Jourdon 2010b: 1709), so this zone was from the beginning financially condemned to dependency. Figures like 56 per cent or 77 per cent seem to make sense because a 60 per cent figure is still controllable, which is less the case with 77 per cent. These figures must also be confronted with strategic examination of how actors behave facing this structural constraint.

1917–2015: US $

From 1917 the United States (not the United Kingdom), became the leader managing loans to the Allies. Actually, before 1945 and the replacement of the pound as the key currency, the system around the £ Sterling, which was an offensive system, became a defensive one. In 1925 the pound devalued 27 per cent. The Americans devoted over 50 per cent of war reparations to France, but the Germans refused to pay ... which awakened sensibilities ... On the other hand, the German currency itself experienced a spectacular collapse in 1923. With the expansion of the global system, came the period of the US $ as the key currency. Compared to the period of £ Sterling as the key currency, when the world system centre was very small, the monetarized countries became a majority in the world (Jourdon 2010b: 1649–1656 shows for some important countries the moment in the 1980s when monetary masses became more important than the private savings). Nowadays, the study of long currency cycles must incorporate new assumptions in its methodological framework. Studying history, one may have a look at the concepts of endogeneity or exogeneity of money with regards to development, economic growth, and expansion of the global system processes pertaining to national traditions involving different accounts of world economic history. British and American sides would have different accounts. And so would French and German traditions bring different accounts, which a posteriori may appear ‘still unborn’ at a given time, but would strongly contribute,to a new – particularly European – future synthesis. Since this new competition began, it seems appropriate to discuss which elements have presided to the takeover. The authority at the forefront of social credibility, the authority with respect to inter-sectorial or intra-sectorial credit, the authority with respect to macroeconomics, the authority concerned by alliance and coordination between nations, should be looked at carefully (Jourdon 2010a: 1130–1132). The impossibility of the return to the gold standard / £ Sterling regime triggers the need to look at beliefs regarding the relationship between the currency and its key underlying hardware. It shows that people tied to money were looking for a trustworthy anchor established in the past, whereas only an anchor chained to the future could afford to build a really operational macro economy (Keynes 1936). This is also why the handover was so violent – the forced passage by the state of war, a quarter of a century long. Compared to the long monetary cycle of 1848–1945, that of 1917–2015 shows that the new key currency was more capable to anticipate: the money reserves in US $ started to be accumulated massively from 1917. From 1917 to 1944, the increase of the United States' currency amounted to + 421 % compared to the three monetary ‘leading’ countries in Europe (France, United Kingdom and Germany). What all the more confirms the theory is that the bulk of the increase occurred at the end of the period: + 193 % between 1938 and 1944, showing that the Federal Reserve Board massively anticipated future needs in the global economy (Jourdon 2010a: 1146–1147). The new context from the 1970s with the conquest of more than half of the world in a monetized or close monetized territory is also studied (see Jourdon 2010a: 1199–1200, 1207, 1224–1227, 1514 for general explanations; Jourdon 2010b: 1637–1640, 1649–1654, 1656, 1701–1705 for data; Ibid.: 1856–1862, 1864–1867, 1869–1870 for diagrams). The de facto solidarity between Europe and the Arab Muslim world by petro dollars and euro dollars, and the simultaneous opening towards East and South to the International Monetary debt, play on. The debt of the centre clogs the system and announces the end of the long monetary cycle: the United States' debt between 1974 and 1992 climbed from 33 to 65 per cent of the national American gross product. Whilst the UK during its monetary long cycle had largely covered the global debt of its ‘allies’ on the periphery and semi periphery, the United States went into debt from the beginning. In the end the central debt goes faster, but the Europeans – at the beginning less indebted – once again reached the same level of debt as in the United States. The situation is different because the monetarized geographical area – compared to that of the entire world – is much wider than it used to be in the past.

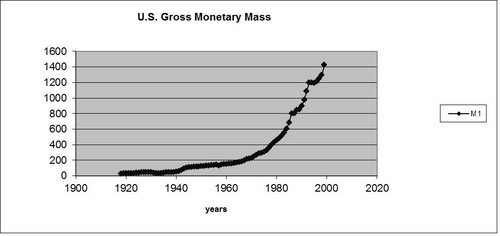

Diagram 3. The consideration of the monetary long cycle of the US $ (1917 – after 2010), monetary mass of US $ (in billion $).

Source: Jourdon 2010b: 1819. Figures can be found at www.fgn.unisg.ch/eumacro/ macrodata/macroeconomic-time-series.html

Commentaries:

- It looks like an S curve – the Diagram 3 shows about 80 % of this long-cycle (which we predict will last until about 2015). It would validate the theory of a monetary long cycle with respect to the US $ (Jourdon 2010a: 1195, 1198–1200). We could also extend the study to US $ + Western European monetary allies (considering the period from 1917 to 1991) (Jourdon 2010b: 1827–1828, 1833–1834). However, in this case, it might tell us more about the tendency (exponential) than about the monetary cycle: for Western Europe has been officially prepared to become a monetary competitor of the US $ since the Werner Plan in 1970.

- A strategic examination of behaviours should combine with statistical regressions. Particularly in the first period (1917–1945), the competition between Europe and the US plays toward exploding the dimension of the monetary mass (Jourdon 2010a: 1140–1142, 1146–1147). Europe is going further than the United States at first, because of Germany's deep monetary troubles. We would also argue about the need for monetary neutrality from the US at this period – like the UK did during the former cycle, trying to give a decisive impulse whilst remaining protected behind the allies for their influence… When World War II ended, the US monetary mass definitely prevailed during a new thirty years' period – as shown in Diagram 3.

- At the end of this long monetary cycle, the relation between the cycle – around the key currency – and the structural monetary environment changed worldwide, because the safety exit is no longer to advise new countries to enter the monetary system, while oneself assuming less new financial risks. It depends more on how to manage the world full of indebtedness (Jourdon 2010a: 1172–1177) … this time even at the end of the monetary long cycle – though a little stabilized since 1992 for instance in France from 1992 to 2005.

Forecasting a monetary long cycle of the euro, from approximately 1992 to about 2090, we would dare to make some suggestions:

– Keynes denied any neutrality to money from a theoretical standpoint. In the future, this position will claim a new practical meaning. For the expression ‘money has no door’, thanks to internet, makes no sense any longer: with internet it is easier to investigate where money is coming from and where it would go. That will have systemic consequences on the link between plain statistic regressions and strategic investigation, that is between the respective investigations of a cycle and of a tendency.

- The econometric question would become more how to find new ways to discriminate quantitative and qualitative data, in order to help formalize building a new monetary system around the need for new goals (notably sustainable justice).

- The means that the new key currency will have to carry on: 1) the allies' choice to fulfil its ambitions; 2) what signs of positive property – not debt – could the Central Bankers put in front of common decisions in order to converge toward specified goals?

- Try to balance the means and goals, with two world constraints: 1) to harmonize the monetarization and the democratization processes; 2) to prevent exhaustion of the planet's natural resources. Maybe, for all these objectives and in order to help the goals be achieved one needs a world account unit, serving as a ‘barometer’ and a ‘metronome’ to help convergences.2

Discussion of the Results in Light of the Theory

Germany was institutionally excluded from the world economic system during the last period of the £ Sterling (1917–1945).

The US $ has also been caught up by debt, but has for a long time resisted due to the enlargement of the global system (and its centre), which dilutes the risk.

The underlying elements of the key currency evolved: it is less and less based on hardware, and increasingly in terms of credit (Dupriez 1966), or even on a more immaterial one, making easier processes of catching up with electronic money. But new underlying guarantees also bring risks of confusion related to the real underlying of funding. The confusion is common in times of crisis between solvency and liquidity.

It is likely that the United States had been anticipating for a long time the future situation in Europe, while the United Kingdom failed to do the same with respect to the United States of America.

What was crucial in the handover between the US $ and the £ Sterling is that between 1917 and 1945, only half of Europe was monetarized (at least northern Europe) and the other half was not monetarized. So, the maximum pressure weighed on Germany that could not manage the problem rationally enough, which led to convulsions.

In order for the key currency to take a full part in the expansion of the global system, it must be supported by a management system of property rights, enabling these property rights to spread on a broader space. This dissemination can be made either from one nation to another or from one sector to another, or by a more or less biased impact between both economic sectors and political nations, for example by the use of special utilities like energy.

In comparison to the first monetary long cycle, the outlet of the cycle is not so violent because nations placed at the end of the system – now Japan – have an interest in the continued expansion of this system, which was not the case at the end of the 1848–1945 period when Germany was at the edge of the system.

The £ Sterling system was oriented towards sale. Germany had tried to build a system focused on purchase. The US $ system was halfway between a sale system and a procurement system. The logic of evolution of the £ to the $ system is also sectorial: as there are henceforth not only two sectors practising monetary exchange (agriculture, industry), but three (agriculture, industry, monetized services), credit spreads in both directions between producer and consumer, and not only from the producer to the consumer.

All in all, the theory seems to be confirmed by examining the periods 1848–1945 and 1917–2015: the key currency linked to the defence of private property led to a social deadlock that convulsed into a war. This statement comes from a review of the status of the global system: at the time of the £ Sterling the centre was basically reduced to Western Europe and also later to America. The choice in favour of economic liberalism and the development of industry and defence of private property: all motivated by a global desire – thanks to this economic development – to push away anarchy of political relations between states (Jourdon 2006). The colonization processes – especially British and French ones – with the stated desire to ‘educate’ the colonized (a desire expressed in France by Jules Ferry) clearly showed the increase of dualism between countries, between the lower and the superior. But this social competition for the creation of money was present also within even the most economically entrepreneurial behaving nations. Thus at that time we can observe a rise in inequalities both internal and external between the nations. Closer to the centre of the global system – located within European borders then – this seems even more striking. It shows that this system defending private property – and therefore having some tendency to evacuate forms of social properties – created imbalances that eventually affected states, and caused political unrest. The European periphery saw its debt growth until the end of the gold standard period, which would lead to riots and violent social movements (the Balkans, from the 1880s). Further on geographically, the system, in order to capture new private property rights related to a monetary system built around the £ Sterling, has completely ousted India and Egypt on international trade. Because these countries would not have accepted gold as money, for they only wanted silver. So the natural outlet of the system at the time was to maximize trade with the currency. But at the system's boundaries, since they were less socially insured, only imbalances were created; and far fewer benefits. Severe conditions occurred during crises in Greece, Portugal and Spain. We deduce that everything was preparing to bring the final operation for the system: it would have been reckoned in order to do away with this long cycle and then to be able to expect a new regulation… a clearing operation between financial risk and political risk. Unlike the definition in the absolute of ‘constructive ambiguity’ of money, the ambiguity between financial and political risk did not appear to be constructive at all at that period of time. For it put balancing more and more risky (because of the debt) financial gains, across the back of political anarchy (due to the threats of social unrest). In continuing to expand with the same management system of property rights – with lots of private property and much less social property (the promises made by Western Europe to the countries of Eastern Europe were primarily financial, so political and thus social counterparts were virtually non-existent) – the system was led inevitably to its financial convulsion. This convulsion occurred in a brutal material, not abstract, fashion, at these geographic boundaries of the system.

During the current, after 1992, period of the monetary long cycle of the US $, we can distinguish a new story. The key currency linked to a private ownership – social ownership balance provides credit, consumption, negotiations around ‘the always more’ as the very goal. It leads to some new forms of system blocking.

It is attempted to get a catching up point to determine on the entire monetary long cycle. Approaching this ‘self-fulfilling prophecy’ in its beginning would help us bring out the moment when the most basic impulses – those on the trend in the world – no longer seemed to come from America but from Europe: since the 1980s.

In the phase of decline ($), the decline of the key currency is operated jointly with the challenger that proves its ability to better manage the expectations of global in-vestors:

- their pace;

- their formulating time;

- how to manage these instructions in a systemic perspective in order to acquire ‘the majority’ in the direction of the system.

In the 1970s the European Economic Community (EEC) regularly lost half the results of its efforts in coordinating monetary policies, because of some speculative frictions on the financial related markets. It constantly had to make concrete efforts to absorb the fluctuations between currencies because of attacks from the dollar ($ devaluations or raising of the U.S. interest rates). As early as the 1980s these friction forces began to be somehow less devastating. The rapprochement between Western and Eastern Europe began to emerge several years before the collapse of the Soviet system.

On the one hand, the USA was better equipped than Europe in terms of the real economy in the production of information technology and communication. On the other hand, monetarily speaking Europe knew an increase in its overall public debt, in order to support growth in a depressed time: however, it was based on fundamentals that were less subject to financial risks than was the case for the United States. Taking into account these conditions, we dare to state that even if financial and monetary competition between Europe and the United States was at its dawn, the underlying institutional monetary sovereignty was already stronger in Europe than in the United States. We mean a healthier way to understand the issues relating to the global symbolic economy denominated as ‘values’.

That is why the impulses have started to come from Europe.

The ‘realistic’ U.S. model of international relations – which would be based on a national/international vision which would combine liberalism at home and prevention of political anarchy outside – will increasingly compete with a ‘Kantian’ model. According to the latter, at home it is the objective to approximate the policy as much as possible to the social goals (rather than purely economic ones), and outside a ‘fuzzy’ management of property rights should prevail, combining conservatism in matters of security, and Utopia in rights to leisure, personal development, education and health, in order to achieve social progress.3

Then the main impulses by Europe had stabilizing effects on the system. First of all, we note the acceleration of European integration made notably by French President Mitterrand and German Chancellor Kohl. Suddenly America, which until that moment was far ahead both in the monetary economy and the real economy, kept the lead for only the real economy. Europe in the 1980s put forward its political influence, overcame its fears of the traditional red communist Hydra, the black Hydra related to migrations, the green Hydra of ecology. Its natural ally in Asia, Japan, seemed geopolitically more influential a power than was the natural ally of the United States that appeared to be China (Japan at this time helped more other Asiatic countries than China did). So since the 1980s thirty years have passed. Still today we find that European monetary impulses are more stable than the American impulse, but nevertheless these latter two continents will have to work together to stabilize the world and to get out of the crisis: they have no choice because both are seriously indebted. Europe would appear more virtuous in the green economy (with less emissions of greenhouse gases per inhabitant), while the American model of economic growth is still heavily dependent on military spending (40 per cent of global military spending). Also, since the 1980s, the first French companies have bought U.S. companies, including those in the very important sectors such as insurance (e.g., AXA Company case), whereas previously it had always happened the other way round. Between green development and military expenditure, the U.S. funding system appears to be based on more speculative revenues. Europe invests moderately but in a more assured way. The financial scandals similar to those that erupted in the United States (ENRON bankruptcy of pensions in the 1980s) did not occur in Europe. Basically in the 1980s Europe began to appropriate the ‘downwind’. We can also quote the Restructuring the International Monetary System by prudential policies (Basel Committee), the Conference on Sustainable Development (Stockholm Summit in 1987), the beginning of a peace process in the Middle East that for the first time in history proposed a political discussion between Israelis and Palestinians (European-based conferences, in Oslo and Madrid), and the last, but not the least, the peaceful democratization process in Russia with Mikhail Gorbachev's Perestroika in 1989. Meanwhile, the United States continued to invest all over the world but by financing risks (real estate securitization), so it is unclear how long term cumulative risks shall be balanced, it will probably require extensive international negotiations. Since the early 1980s the United States have benefited from an outside banker – China. But politically they eventually decided a progressive withdrawal from a growing number of Latin American countries. It is too early to assess that a new, truly European macroeconomic model has to be imposed. But if it is announced, its impulses are symbolic targets for all the humanity. This was ensured by a stable monetary system in its operation, though quite immature still in its institutional recognition.

This last paragraph analysis is made on qualitative data. But to show that the account is useful, it is also necessary to find the very rhythms of this ‘world social evolution’, which is financed ambiguously by this complex key currency.

It is not enough to discuss the results in light of the theory as the examination of the first two monetary long cycles – from 1848 to 1945, and from 1917 to 2015 – seems to corroborate the theory. But it seems also interesting to deepen and extend the theory using the results. The argument itself presupposes to think over the taken together long monetary cycle and trends related to the world social evolution. This is especially true with respect to the future, because we have to bring together monetization and democratization processes.

Theoretical Conclusions

To think of the coming monetary cycle one should consider in a new way the relationships between economic sectors, between major regions and/or nations, and between sectors, on one hand, and regions/nations, on the other hand. It makes sense to build the model to point out an evolution of the orientation within the management system of property rights attached to the key currency. The new key currency would or could be structured, so as to meet the requirements of these moving relationships. Also, during the period from 1945 to nowadays, the macro economy was built to integrate social aspects more than before. It is unlikely that this will change; in the frame of the analysis of our changing social world, the global system centre would logically export its models to the rest of the world. To go forward it would rather expand its operational mode to integrate new features enhancing its time consistency, such as sustainable justice.

Harmonization between European and American rhythms seems necessary to draw a new fiscal value from the reserve currency, take advantage of interactions between a purely monetary economy and a purely symbolic and human economy to ensure the system. Eurasia, whose economy would be rather real and dependent on a true relational logic with its customers – as a yuan still pegged to the dollar would demonstrate – will be in that context a useful reminder of reality for Europeans and Americans, in order for them to reach agreement, if we state the American economy is rather a monetary and insurance driven one – ceteris paribus – and the European one would appear rather human (sometimes a ‘symbolic’ one when we think of the controversies in its social model).

Europe, by managing at best a global ‘constructive ambiguity’, which would result from frictions between Asia and America, appropriates both the insurance capacity of the monetary system, and a part of the capacity responsiveness of the logistics system. It could eventually, through its currency, embody the ‘new dream’ which represents the ‘symbolic power’ associated with a desired future state of the world meaning a true dialogue of civilizations.

General Conclusions

We supplement Marjolin (1941) and Dupriez (1966) theories of long monetary cycles with a specific content for the 21st century. Dupriez went further than Marjolin in two determining items: 1) the nature of money: it may largely rely on credit circulating in the economy and be created as needed by the foremost commercial banks; 2) Dupriez also stated that the long monetary cycle must achieve social development for centuries. He linked the social, human, and even the deep collective psychology, to the macro economy. By linking the internal (social), external (geopolitical), and contingent (economic) dimensions, we chart a general access path opened up to all future economic theories. Subsequently it will serve for numerous applications, for instance, any scheme of precautionary risk management in Eurasia.

The basic point of the method which should serve political negotiation is that, from the time when half the countries and peoples have their system organized according to criteria derived from the cash economy and not the real economy, the world must be organized according to such a framework. It is urgent and important to formalize new general criteria for economic science considered, for instance, by Sen (1999) as a ‘moral science’. Our model will help to establish foundations for sustainable macro economy, preventing conflicts, making ‘sustainable justice’ (Strauss-Kahn 2004) triumph. This is all the more relevant now, that more than half, of both peoples and states, are now democratic regimes.

We point out three directions to sketch a new theory of sets that will help us to build credible models and advise clearer, more pertinent decision-making process.

- A theory of long monetary cycles (Jourdon 2010a) with an announced social project backed by euro + the world system + the double recognition that today more than half of both peoples and states live in the context of monetarized economies and in a democratic political system (Jourdon 2010c), enables us to outline a new monetary theory.4 This theory may be put into equations considering the time dimension of the monetary long cycle, and two or three geographical or social items moving together in accordance with that time dimension. The latter will be ‘customers’ throughout the announced monetary cycle, of the institutions in charge of such complex governance, in a very complex negotiated framework – a part of new consensual perspectives (Tausch 2006).

- Before Keynes, the typical ‘general model’ of economic policy was centred on the real economy, symbolized by the General Equilibrium Model of Walras (1889). From the monetary long cycle related to dollar, the general model of political economy has been a macroeconomic model, first conceived by Keynes and formalized by Hicks (1937) and Hansen (1949), then complemented by all successive macroeconomists. Today, one would need a model of ‘sustainable macro economy’: preventing conflicts, rooting macro economy in justice, democracy, and environment protection. In the first period of its existence, the theory had privileged savings, and then the second period put forward the concept of macroeconomic money. Now it seems necessary to study the twisting fiscal phenomena and relate them to external effects related to power. Their endogenous making in a pattern that would take conflict as input and justice as output, everything under constraint of peaceful means, should be studied.

- The directions displayed might prelude reconciliation between monetarist, Keynesian and neo-Marxists monetary theories.

Thus, one can glimpse some space for debate where it will be possible to talk about ‘from local conflicts to a comprehensive peace’ (Chistilin 2006).

The unavoidable feature in the study of money remains the ‘constructive ambiguity’. Adding to this study the emerging constraint of ‘participatory democracy’, will usefully recall the horizon of the social change. In the current world crisis, for the first time in history the question is raised of a worldwide tax problem. Our framework is fitted to a progressive better integration of social capital and human capital aspects, linked with monetary issues. Only this kind of perspective could solve the tax problem, allow convergences, avoid useless legal conflicts, and even worse conflicts, in the situation of generalized indebtedness.

NOTES

1 We refer to the year 1848. Our reasons reflect a strategic choice of British money directors. From our figures, monetary mass + private savings climbed from 1817 to 1848 from 28.7 to 50.6 millions of £ Sterling, that is about +76 % during 31 years. From 1848 to 1873, the same masses climbed from 50.6 to about 100.3 (in constant £ Sterling): + 100 % in 25 years. If we think of the monetary long cycle as a feature purely internal to the United Kingdom, we would have estimated its beginning before 1848, but it would not make sense to qualify it as a monetary long cycle that way, because such a feature is of international nature, both legal and effective. We took the beginning date when the phenomenon became clearly internationally cross-emulated and related. 1817–1848 would be more a ‘proto-period’, preparing the monetary long cycle. The question when to start a monetary long cycle is one of strategic obedience. For the Central Bank, it is essential a balance between private savings (i.e., on the financial markets) and monetary mass (which strongly influence the global official national currency positions) in order to secure margins of negotiation. We mean inner margins between public debt, financial markets, and the national currency position, and outer margins between the £ Sterling position and other countries' currency positions, which could not officially exist before the creations – in 1848 – of the French and of the Russian Central Banks, and even before 1871 taking into account the creation of the German Central Bank. These margins of negotiation are necessary in order to explain these dynamic long-term (for almost a century) historical phenomena. They fund the secular social development. Institutionally only then will it rely on background flexibility of negotiations, which bring positive external effects for key currency sovereignty with them… After 1848 we can see at work the ‘constructive ambiguity of money’, the core of money's nature.

2 Since the financial crisis of 2007–2008, many observers of the International Monetary System noted that a project on the full development of the euro – competition between € and $ to become the primary reserve currency in the world – is no longer relevant because the light of globalization or even widespread debt problems should be a global currency. I would like to reply using two directions and showing a conclusion. 1) Competition between the euro and dollar is a natural process, but can happen in a negotiated manner. To avoid brutal regulation, it is necessary to define the new challenges to a long-term development model for humanity, taking into consideration all risks related to sustainable development: global warming, energy crisis, food outlook, growth in world population in relation to the number of available jobs to be filled, and migration issues. Then we would try and anticipate crises and see how currencies can provide a better management system on the global scale over a longer time term. Hence a new doctrine to reconstruct the relationship between national – or regional related to 15 to 20 main regions in the world after the UNO Report on the future of the world economy (Carter, Leontieff, and Petri 1977) – security, economic sectors' interests, philosophical values of social classes. We leave the door open to margin adjustment from ‘private currencies’ providing their services. 2) The question of a global currency is no new idea. Keynes proposed it in 1945, calling it ‘bancor’. Today, we would find it rather unrealistic, primarily as that currency should be backed by a social project in this case a global one. This could not be done right away because we still suffer the consequences of Social Structures of Accumulation in the previous period from 1945 to the early 2000s (Edward, Gordon, and Reich 1994) built on strong implicit discrimination forms like sexism and racism. The question of a key currency, even more the question of a world currency, is inseparable from both an accepted and shared social project (to out-pass every phenomena of discrimination real or implied) and a system of penalties ensured by independent authorities responsible for enforcement of these rules. 3) The question of a world currency would seem though relevant as long as principles can be designed to neutralize up to its flexibility as both a standard of exchange, store of value, unit of account. It should only serve as a unit of account in order to frame a list of negotiations. It would, dynamically, be in charge of accounting change ... It would serve as both a barometer and a metronome and allow negotiations during the institutional transition from a key currency to another. It would provide compensation means, like systems of points to be refunded or to win, marking models that would provide for a balance between generalized data of real nature, monetary nature and symbolic nature (related to philosophical, human, social values). Such items would exist for each major region backed by a monetary area. Such a global unit of account would be complementary to the key currency, whose ambiguity is to be ‘double-sided’: one side is open to private commercial interests, and the other side is publicly defending the social interest. So the four targets are: 1) world currency: unit of account; 2) key currency (symbol of social project and ‘the New Dream’); 3) private currencies for adjustment services, manage their own patrimony, micro-innovations…; 4) independent authorities to defend sustainable justice everywhere.

3 Resulting out of interest rates, exchange rates. Compared with the dominance of time that is of the United States, the outsiders are trying to recover a partial domination of the area controlled by the U.S. hegemonic system. As long as the dollar was unchallenged, it was, contrary to the £ Sterling's situation in its heyday (a ‘vertical-type’ operating currency ruling in an authoritarian way on time thanks to the discount rate), a ‘horizontal-type’ operating currency. An ‘innovation’ in the international monetary system was a currency for a subsided geography, a real spearhead for the triumph of a system based on ‘freedom’. Values were transmitted with a real generosity towards old Europe. The financing system focused on the growth of symmetrical relations between Europe and America prevailed. A management-system of merchandise money/oil commodity, vs. credit money, was put into force close to Europe and Africa. The development of a third pole to the extreme Eurasia (Japan and its few protected countries) was agreed. And ‘containment’ ruled elsewhere: authoritarian in Latin American countries, ‘dry’ in Africa (no credit allowed), and a diplomatic containment around the Eastern bloc. Freedom was jealously ‘looked at’: maximal at home, much less elsewhere. Since the dollar felt being threatened, everything changed! Then the dollar was no longer a ratio for rights' broadcasting. It newly represented a ratio of voltages.

4 See Endnote 2.

REFERENCES

Aglietta, M.

1979. La notion de monnaie internationale et les problèmes monétaires Européens dans une perspective historique. Revue économique 30(5): 808–844.

Aglietta, M., and Orléan, A.

1998. La monnaie souveraine. Paris: Editions Odile Jacob.

Carter, A. P., Leontieff, W., and Petri, A. P.

1977. The Future of the World Economy: A United Nations Study. Oxford: Oxford University Press.

Chistilin, D.

2006. Principles of Self-Organization and Sustainable Development of the World Economy: From Local Conflicts to Global Security. In Devezas, T. (ed.), Kondratieff Waves, Warfare and World Security. Vol. 5. NATO Security through Science Series: Human and Societal Dynamics (pp. 100–108). Amsterdam: IOS Press.

Dupriez, L.

1966. Des Mouvements Généraux de l'Economie. 3ème ed. Paris: Béatrice-Nauwelaerts.

Edwards, R., Gordon, D., and Reich, R.

1994. Social Structures of Accumulation. The Political Economy of Growth and Crises. Cambridge: Cambridge University Press.

Flandreau, M., and Le Cacheux, J.

1997. Dettes publiques et stabilité monétaire en Europe. Les leçons de l'étalon or. Revue économique 48(3): 529–538. URL: http://spire.sciences-po.fr/hdl:/2441/9labe9r4se65i 789685q56g16?time=triptych &sortColumn=dateIssued&sortDir=desc&start=100.

Friedman, M., and Schwartz, A.

1982. Monetary Trends in the United States and the United Kingdom. Their Relation to Income, Prices, and Interest Rates, 1867–1975. Chicago – London: The University of Chicago Press.

Hansen, A.

1949. Monetary Theory and Fiscal Policy. New York: Mc Graw-Hill.

Hicks, J. R.

1937. Keynes and the Classics; A Suggested Interpretation. Econometrica 5(2): 147–159.

Jourdon, Ph.

2006. Wars on the Borders of Europe and Socio-Economic Long Cycles. In Devezas, T. (ed.), Kondratieff Waves, Warfare and World Security. Vol. 5. NATO Security through Science Series: Human and Societal Dynamics (pp. 165–172). Amsterdam: IOS Press.

2010a. La monnaie unique européenne et sa relation au développement économique et social coordonné: une analyse cliométrique. Tome III. Modèle et calculs: une théorie monétaire des Cycles de Kondratieff, l'Euro de 2000 à 2050. Entelequia, Málaga. URL: http://www.eumed.net/entelequia/es.lib.php?a=b012.

2010b. La monnaie unique européenne et sa relation au développement économique et social coordonné: une analyse cliométrique. Tome IV. Annexes. Entelequia, Málaga. URL: http://www.eumed.net/entelequia/es.lib.php?a=b013.

2010c. Le nouveau cycle long monétaire implique une nouvelle façon de gérer l'économie d'entreprise et réguler l'économie politique. Sciences Sociales et Humaines 2(1). URL: http://www.middle-east-studies.net/?cat=152.

2011. A New Theory of Monetary Long Cycles, with Assumptions Fitted to the Twenty-first Century. Journal of Globalization Studies 2(1): 97–112.

Keynes, J. M.

1936. Théorie générale de l'emploi, de l'intérêt et de la monnaie. Paris: Bibliothèque Scientifique Payot.

Marjolin, R.

1941. Prix, monnaie et production. Essai sur les mouvements économiques de longue durée. Paris: PUF.

Mitchell, B. R.

1992. International Historical Statistics: Europe 1750–1988. New York: Stockton Press.

Sen, A.

1999. L'économie est une science morale. Paris: Editions Repères La Découverte.

Strauss-Kahn, D.

2004. Construire l'Europe Politique – 50 propositions pour l'Europe de demain. Rapport pour le Président de la Commission Européenne.

Tausch, A.

2006. From the ’Washington‛ towards a ’Vienna Consensus’? A Quantitative Analysis on Globalization, Development and Global Governance. Paper presented for the discussion process leading up to the EU-Latin America and Caribbean Summit 2006, May 11–12, Vienna, Austria. URL: http://www.caei.com.ar/ebooks/ebook1.pdf

Walras, A.

1889. Eléments d'économie politique pure (ou théorie de la richesse sociale). Paris: Guillomin & Cie.

Appendix

Monetary mass + savings related to the £ Sterling: increased by 50% between 1848 and 1860

|

|

Monetary mass (Banknote Circulation) – millions of £ Sterling |

Savings (Deposits in Savings Banks) – millions of £ Sterling |

Total Monetary Mass + Savings |

|

1847 |

19.1 |

30.3 |

49.4 |

|

1848 |

18.1 |

28.2 |

46.3 |

|

1849 |

18.4 |

28.6 |

47 |

|

1850 |

19.4 |

28.9 |

48.3 |

|

1851 |

19.5 |

30.3 |

49.8 |

|

1852 |

21.9 |

31.8 |

53.7 |

|

1853 |

22.6 |

33.4 |

56 |

|

1854 |

20.7 |

33.7 |

54.4 |

|

1855 |

19.8 |

34.3 |

54.1 |

|

1856 |

19.7 |

35 |

54.7 |

|

1857 |

19.5 |

35.2 |

54.7 |

|

1858 |

20.2 |

36.4 |

56.6 |

|

1859 |

21.3 |

39.2 |

60.5 |

|

1860 |

21.3 |

41.5 |

62.8 |

|

From 1861 to 1869 – yearly average |

21.9 |

45.6 |

67.5 |

|

1870 |

23.3 |

480.4 |

503.7 |

|

1871 |

502 |

531.2 |

1033.2 |

References and Sources: Banknote circulation from 1848 to 1860: Mitchell 1992: 764–766. Monetary Mass in 1871: Friedman and Schwartz 1982: 130. Deposit in Savings Banks from 1848 to 1869: Mitchell 1992: 780; in 1870–1871: Ibid.: 783. Deposits in Commercial Banks in 1870–1871: Ibid.: 773. Banknote Circulation can seem an approximation of Monetary Mass at this period. We only take Banknote Circulation by Central Bank. Banknote Circulation was made by Central Bank solely during a long time period, according to Mitchell. It is mentioned also banknote circulation coming from commercial banks since 1833, almost as important as the amount produced by the Central Bank (2/3 of it), and after 10 years regularly half of Central Bank production produced by commercial banks. After 1870, the compared amount of banknote circulation by commercial banks was still reduced, about 1/3 of the quantity by the Central Bank. We estimate savings as the savings in Savings Banks. There could be also a part of savings in commercial banks. We estimate our technical appreciation fits two criteria: 1) evolution of more institutionally recognized means of payment in regard of the coming role of £ Sterling as a key currency; 2) consideration of means of payment which can serve as reserves of value (not only as a standard for exchange). We come to our approach that seems to us relevant in order to account for true monetary signs. To be fully exhaustive would have implied also quoting the reserves in precious metals. We neglected that because the philosophy of Central Bankers at that time in England was more to have a kern to support for global speculation and forecasting, rather than accumulating ostensible money. Otherwise, this relative negligence is strictly symmetric with our neglect of savings in commercial banks. These financial effects seem to us – ceteris paribus – more related to commercial credit than to civilly opposable – in absolute terms – money. It is possible that Friedman and Schwartz (1982) include deposits in commercial banks in their Monetary Mass. It would be historically defendable because suddenly there was the new competition for monetary influence on the continent, because of the creation of the German Bundesbank. The United Kingdom profited from that event to make a legal devaluation (1 £ Sterling becomes 10 new £ Sterling). Anyway, Mitchell does not quote deposit in commercial banks before 1870 (common operations with France may also have created this boom). Deposits in commercial banks: in 1870–1871, a very important amount: proof that this new role of commercial bank for institutionalizing their credit was prepared for a good time, sign of a perfect synchronization between British players and customers.

Размещено в разделах