The Rise of China, New Patterns of North-South Trade in Natural Resources and Their Impacts on Standards: Evidence from the British Columbia Forest Products Sector

скачать Авторы:

- Bowles, P - подписаться на статьи автора

- MacPhail, P - подписаться на статьи автора

Журнал: Journal of Globalization Studies. Volume 5, Number 2 / November 2014 - подписаться на статьи журнала

The growth of Asian developing countries and China in particular, has changed patterns of world trade. One example of this is an increasing natural resource export from northern (high-income) countries to southern (low-income) countries. The shift in the export of natural resources to southern countries raises questions about whether this also leads to a shift in standards as a result of the lower standards and weaker enforcement of standards in the southern countries now demanding natural resources. We address this issue by examining exports of British Columbia forest products over the past decade where there has been a clear export market shift from the USA to China over this period. We conclude that, because of the production characteristics of the forest product sector, to date there has been no shift to lower standards as a result of the shift in the direction of trade toward China. In fact, the general case is that producers meet the standards set in the highest importing market: a reversal of the more usual ‘race to the bottom’ hypothesis.

Keywords: North-south trade, natural resources, forestry products, standards, China, Canada.

1. Introduction

The growth of Asian developing countries has changed patterns of world trade over the past two decades (Kaplinsky 2005; Henderson 2008). This can be seen as the latest development in a century-long international division of labor. In brief and in general, the colonial international division of labor, which lasted until the 1960s, consisted of commodity (or natural resource) exports from the south and manufactured exports from the north. This was followed, from the 1970s onwards, by the shift of manufacturing production to the south and rising manufactured exports from south to north. In the 2000s, in the context of a global commodities boom, parts of the south have become major commodity importers from countries in both the south and north. Northern countries had previously been commodity exporters but predominantly to other northern countries; now the south is an increasingly important market. One example of this latter trend is increasing natural resource exports from Canada to China. Whereas Canadian exports previously went to other northern countries, most notably to the United States, there has been an increasing shift towards new markets in the south, most notably China.

Shifts in global trade and in the international division of labor are often accompanied by changes in the standards intensity of production. For example, the 1960s and 1970s shift of labor-intensive manufacturing from northern countries to the southern ones was accompanied by what many regarded as a ‘race to the bottom’ in environmental and labor standards, given the lower standards and weaker enforcement in the countries of the south now producing the manufactured goods. It was not that trade caused a direct change in standards but that the overall standard intensity of global trade declined as investment and production increasingly relocated to countries with lower standards. This resulted in a wide debate about the case for including such standards in global and North-South trade agreements (see, e.g., Barry and Reddy 2008; Busse 2004) as a way or limiting this trend.1 In the 2000s, the shift in the export of natural resources to southern countries raises questions about whether this also leads to a shift in standards as a result of the lower standards and weaker enforcement of standards in the southern countries now importing natural resources. In this case, the standards intensity of trade would again be lowered but now the changed export destinations might be expected to change standards directly as producers sell to lower standard consumers; Kaplinsky, Terheggen, and Tijaja (2011), for example, argue that this is already occurring for southern exporters.

This paper is a contribution to that topic by examining natural resource exports from a northern country. We examine the case of forest products from British Columbia (B.C.), one province in Canada, where there has been a clear export market shift from the USA to China over the past decade. We analyze how this trade shift has affected product and process standards in the forest products industry.2 This case study also provides valuable insights into the role of standards governance in world trade since, in the forest products industry, the voluntary and mandatory standards are set by a combination of industry, NGO, and government. If standards are being affected by new trade patterns it is important to know which standards are being bypassed or amended. Such impacts have implications for a variety of civil society organizations and governments seeking to promote environmental sustainability and good labor practices, as well as for firms which make strategic decisions about the interrelationship of exports and production. The forest products sector therefore provides an opportunity to analyze the complex interaction of changing global trade flows and the multilevel governance of standards.

In the next section, we provide a brief overview of China's global emergence as a major commodity importer. As an example of this, we demonstrate the shifts in B.C.'s export destinations over the past decade with a focus on the forest products sector where a clear ‘China shift’ can be seen. In Section 3, we provide an analysis of the impact of this shift on product and process standards based on interviews with senior managers of leading firms in the forestry sector, derived from data collected using a semi-structured interview guide. Given that we consider a variety of both product and process standards, the impact of trade on standards cannot be readily examined using a quantitative approach with firm level data. Our analysis finds that, because of the production characteristics of the forest product sector and in particular the integrated production process which means that products are not separated by market destination beforehand, to date there has been no shift to lower standards as a result of the shift in the trade direction towards China. In fact, the general case is that producers meet the standards set in the highest importing market; a reversal of the more usual ‘race to the bottom’ hypothesis. We conclude by summarizing the conditions needed for this result to continue to hold.

2. China's Rise, Global Commodity Trade and B.C.'s Export Shift

It is widely recognized that China's growth has changed global commodity markets. For example, the United Nations Conference on Trade and Development (UNCTAD 2013: 13) notes that ‘the increasing demand for commodities in rapidly growing developing countries, notably China, and the resulting higher price levels of many primary commodities, signifies a structural shift in physical market fundamentals’. Roache (2012: 3), in research prepared for the IMF, reports that ‘China is a large consumer of a broad range of primary commodities. As a percent of global production, China's consumption during 2010 accounted for about 20 per cent of non-renewable energy resources, 23 per cent of major agricultural crops, and 40 per cent of base metals. These market shares have increased sharply since 2000, mainly reflecting China's rapid economic growth’. Some, such as Grinin (2011), have seen China's growth model as extensive and heavily reliant on the increasing use of natural resources.

China's economic rise resulting in substantial increases in China's share of global consumption of major commodities has been achieved through increases in imports in many commodities. The World Trade Organization (WTO 2013: 53) reports that in 2012 China overtook the USA to become the second largest global importer of fuels and mining products after the EU. According to the U.S. estimates, China overtook the USA to become the world's largest net oil importer in September 2013 (see Rehn 2013) and is already the world's largest importer of iron ore and soybeans.

This new pattern on global commodity trade has affected both southern and northern commodity producers. For example, it has led to debate over ‘a re-primarization’ in Brazil (Cypher 2007) and to analyses of ‘land grabbing’ in countries in Africa and elsewhere (Borras et al. 2010). It has also affected northern countries such as Canada, Australia and New Zealand, as the share of their natural resource exports going to their traditional Northern markets has fallen and that of China increased. It is this latter shift in North-South commodity trade on which we focus here.

China's growth has affected many global commodity markets, including forestry. The U.S. International Trade Commission, reporting in 2006, noted that ‘the rapid expansion of China's paper and wood processing industries has required a steady increase of imports of forest products input materials due to China's limited domestic forest resources. This demand significantly changed the pattern of global forest products trade between 1995 and 2004’ (U.S. International Trade Commission 2006: 4–1).

This changed trade pattern has continued since and is clearly evident in B.C., Canada's most Asian-trade dependent province.3 In 2001, 70 per cent of B.C.'s total exports went to the U.S. with 21 per cent going to Pacific Rim countries.4 Just a little over a decade later, in 2012, the U.S. share of B.C.'s exports had fallen to 44 per cent and the Pacific Rim share had reached an equal share at 44 per cent. Within the Pacific Rim, the main country destinations are Mainland China, Japan, and South Korea which combined took 37.6 per cent of B.C.'s exports in 2012.

This dramatic decade long shift in direction of trade away from the USA and towards Asia is even more pronounced when considering the forest products sector. This sector consists of three parts: softwood lumber, pulp and paper products, and other wood products (with the most important being, in order of importance in 2012, raw logs, panel products, and selected value added wood products).

Forest product exports have traditionally been B.C.'s single largest export product. In 2001, this sector accounted for 47 per cent of B.C.'s total exports although its share fell to 33 per cent in 2012. The falling percentage of forest products in B.C.'s total exports is the result of both an increase in the absolute value of some other export categories (especially coal and metals) but also of an absolute decline in the value of some forest products, especially softwood lumber as a result of the U.S. housing market slump. Even so, forest products sector remains the largest component of B.C.'s exports.

The focus of the remainder of this paper is not on the changes in total exports but on the changes in the destination of forest product exports. The export destination is documented for each of the three forest product categories identified above. The purpose is to illustrate the ‘China shift’ in each of B.C.'s forest product exports in order to provide the context for the analysis of the impact on standards presented in Section 3.

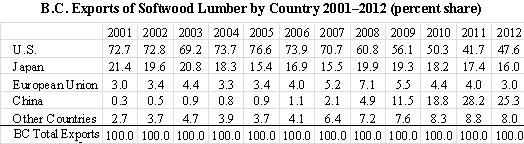

2.1. Softwood lumber

Table 1 below shows the export market shares of B.C.'s softwood lumber for the period from 2001 to 2012. The dramatic rise in exports to China is reflected by the fact that in 2001, China accounted for only 0.3 per cent of B.C.'s softwood lumber exports. This grew steadily to reach 2.1 per cent in 2007, 4.9 per cent in 2008 and an astonishing 25.3 per cent in 2012.

Table 1

Source: Authors' compilation from B.C. Stats, international trade data.

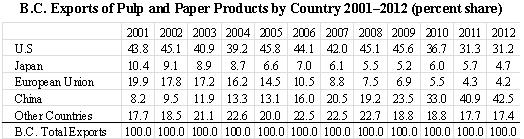

2.2. Pulp and paper products

For B.C. pulp and paper products, China now surpasses the USA as the most important export market. Over the 2001–2012 period, the U.S. share in B.C.'s exports in this product category fell from 43.8 per cent to 31.2 per cent while that of China rose from 8.2 per cent to 42.5 per cent as shown below in Table 2.

Table 2

Source: Authors' compilation from B.C. Stats, international trade data.

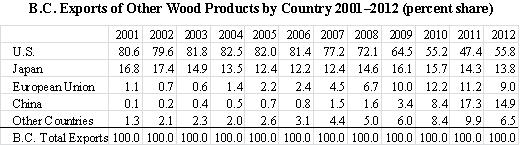

2.3. Other wood products

As noted above, ‘other wood products’ include, in order of importance in 2012, raw logs, panel products, and selected value added wood products. At the beginning of the 2000s, the USA accounted for over 80 per cent of B.C.'s exports of other woods products with Japan taking a further 16.8 per cent. China took only 0.1 per cent in 2001. By 2012, however, China had replaced Japan as the second most important market accounting for 14.9 per cent. Japan's share had fallen to 13.8 per cent meaning that these two Asian markets accounted for close to one third of the B.C. exports. Meanwhile, the USA share fell to just over half at 55.8 per cent. See Table 3 below.

Table 3

Source: Authors' compilation from B.C. Stats, international trade data.

3. Standards and Evidence from the ‘China Shift’ of the B.C.'s Forest Product Sector

As demonstrated above, over the past decade there has been a dramatic shift in B.C.'s trade patterns with the declining importance of the USA as an export destination while the importance of the Pacific Rim and, particularly, Asia increases. This shift is clear for the forest products sector, the province's historically most important export earner. In the case of forest products, though, the shift is a more narrowly focused on one country, namely, China. In all three sub-categories of forest products, the importance of China as an export destination has grown dramatically over the past decade. From low, often very low, levels China has now become the largest single export market for pulp and paper products and the second largest for softwood lumber and other wood products. The China shift is evident and provides a good case study to examine the impact of shifting markets on standards, and in this case a shift to a southern country market of northern country (natural resource) exports.

The impacts of this shift can be analyzed both quantitatively and qualitatively. Quantitatively, the impact of the China shift is quite straightforward. In the face of declining demand from the USA, the increase in the demand from China has saved a significant part of the industry from shutdowns, layoffs and, in all probability, bankruptcies (Peebles 2012; interviews with forest product firms). But while these quantitative effects may be reasonably straightforward and positive, the qualitative impact is more difficult to gauge and raises a number of issues concerning the long-term trajectory of the industry. These issues arise within the broader context of the increasing importance of southern or developing country markets in the global economy.

This trend has been recognized by many and it is variously characterized as a ‘multi-speed world’ (Spence 2011), a Global-Asian era (Henderson 2008), or the Pacific/Asian/China Century (see Scott [2007] for critical review). The aftermath of the Global Financial Crisis has reinforced this trend (Kaplinsky and Farooki 2010). While the implications of Asian, especially Chinese, investment for other southern countries has been extensively analyzed (see Jenkins et al. [2008] for Latin America and the Caribbean and Kaplinsky and Morris [2009] for sub-Saharan Africa), there is somewhat less literature on trade and less still on the trade implications for northern resource exporters, an example of which we analyze here.

In providing an analysis of the implications of the rising importance of demand from the relatively low per capita income countries, China and India, Kaplinsky and Farooki (2010: 18–19) make two key points. The first is that, for southern importers, imported inputs will not be standards intensive and the second is that there will be a growth in imports of relatively unprocessed products. While this may provide some opportunities for southern exporters, it raises the question of whether northern exporters will experience a tendency to reduce standards and whether their product lines will move down the value chain as they export more to low income countries. We concentrate on the first issue here and now move to a discussion of types of standards.

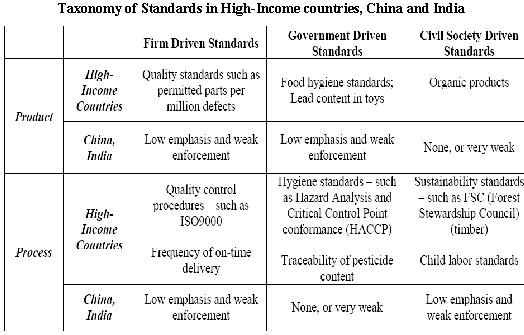

3.1. Standards Framework

As Kaplinsky and Farooki (2010) note, standards cover two dimensions, product and process, and arise from three sources: firms, governments and civil society. Products standards refer to characteristics designed to ensure that a product is of uniform standard while process standards refer to range of technical and ethical concerns for the way in which the product is produced. Firms themselves may be the leaders in some of these initiatives in order to obtain and enhance their competitive advantage in the marketplace. Governments may set regulatory standards, for example, to protect consumer health, and these are mandatory standards. Civil society organizations may be a standards driver in areas such as environmental protection, and adoption of these standards will be voluntary.

Both product and process standards are likely to be much higher for products sold in northern markets than they are in, for example, China and India. Each of the three sources of standards is likely to be much weaker in the latter countries than in northern countries. As Kaplinsky and Farooki (2010: 18) explain, in China and India,

firms are less concerned with product variety, so that the imperatives to achieve flexibility through just-in-time production … are weak. Governments may either have poorly developed safety standards, or fail to implement them effectively. … Finally, NGOs which have driven public opinion on issues such as Fair Trade, labor standards and the environment are muted in low-income countries and are likely to have little significance with regard to the incorporation of ethical and environmental standards in value chains.

These differences are summarized by Kaplinsky and Farooki (2010: 18) in a figure which is reproduced as Table 4 below.

It has long been recognized that northern firms investing and producing in developing Asian and other southern countries are less standard intensive than those same firms investing and producing in northern countries. Indeed, this is much of the rationale for investing overseas in the first place and results in the so-called ‘race to the bottom’ in standards. But while there has been much research on how changes in the location of investment has changed the standards intensity of global trade (see, e.g., 2003, on this for the case of labor standards and investment in China), there has been less research on the impacts on standards of shifts in trade patterns for countries exporting to markets with different standards.

Table 4

Taxonomy of Standards in High-Income countries, China and India

Source: Kaplinsky and Farooki (2010: 18).

Especially interesting for this paper, therefore, is the study of the Gabon timber industry analyzed by Kaplinsky, Terheggen, and Tijaja (2011) where the market shifted from France as the major market destination to China. Gabon, the largest African exporter of timber to China, now exports more by volume to China than to France and equally on a value basis to the two countries. The result of this shift in export market from a high standards importing country (France) to a low standards importer (China) has, according to Kaplinsky, Terheggen and Tijaja (2011: 1186), been that ‘the transition in market destination has led to a collapse in the standards required of producers’.

But if this is the case for southern producers shifting exports from northern to southern markets, is there any effect on standards when northern producers shift exports from northern to southern markets? In this case the gaps in standards are much larger, and hence in this sense under greater threat, but in another sense are less problematic given the pressures that northern countries face from their own citizens and in other markets for the maintenance of high standards. How these dual forces play out in practice has received little attention. This is the case we examine for forest products.

A ‘collapse’ in standards as described in the Gabon case would not be possible in B.C. since the forest industry is subject to various provincial government regulations which provide a floor to standards in many areas including environmental standards and silviculture requirements. These standards are embodied in the 1995 Forest Practices Codes and other legislation. It is true that the standards have been the subject of debate, with critics arguing that they have been weakened by the increasing reliance on company self-monitoring as a result of current neoliberal policies which has seen a retrenchment in forest inspection capabilities (see Parfitt 2010). The weakening of these mandatory standards is, however, not due to a shift in the destination market but is the result of domestic policy choices.

Notwithstanding the fact that the domestic legislation provides a standards floor, it is clear that regulations in importing countries, as well as civil society organization certification, continue to play an important role in influencing the standards compliance of forest companies. We focus here, not on provincial regulations, but on these international factors – as set by international industry codes, importing country governments and by international NGOs – and the importance of which may change as the direction of trade changes. Furthermore, it is not our purpose here to examine whether certification processes, whether by non-state actors or by governments, are adequate and appropriate (see, for example, McDermott 2012 for criticism of the Forest Stewardship Certification process) but to examine whether shifting to the China market affects the application of the certification standards.

In short, we adapt the general standards taxonomy advanced by Kaplinsky and Farooki (2010) presented in Table 4 above to the B.C. forest products industry. The salient points for subsequent discussion are summarized below in Table 5.

Table 5

Framework for Analyzing the Impact of B.C. Forestry Product Exports

to China on Standards

| Type of | Location | Source of standards | ||

| Firm | Government | Civil Society | ||

| 1 | 2 | 3 | 4 | 5 |

| Product | B.C., U.S. | North American lumber grades and pulp grades |

|

|

| China | Modify North American |

| Low | |

| 1 | 2 | 3 | 4 | 5 |

| Process | B.C., U.S., |

| B.C./U.S. Building codes B.C. Forest Practices Code Employment, health and safety standards U.S. Lacey Act California Area Resource Board – | Forest Stewardship Council Programme for the Endorsement of Forest Certification |

| China |

| Building codes | Low

|

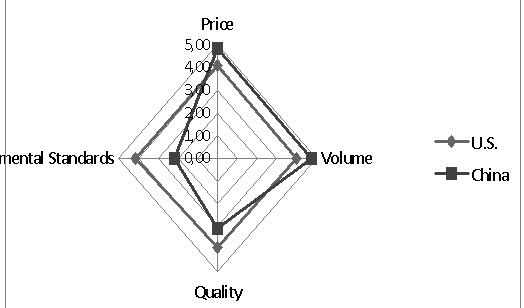

The information presented below which explains Fig. 1 was obtained through interviews with key representatives in the industry. Specifically, we interviewed senior executives from eight firms engaged in all three parts of the forest products sector identified earlier. In addition, we interviewed a senior labor leader representing workers in one part of the industry. The interviews utilized a mixed method approach in which respondents were asked to provide numerical scorings for some questions on standards and provide descriptions of their production processes, and changes in them over time, in response to other questions. The advantage of this method, and the inclusion of qualitative data, is that it enables us gather information on a wider range of processes and analyze causes of changes in them than it would be possible if using purely quantitative measures. The forest products sector in B.C. is highly concentrated and the firms in our sample include the major companies operating in the three parts of the forestry sector in B.C.5

As a preliminary investigation into whether the change in trade direction might potentially affect firm's behaviour and standards, we asked the senior executives to score the importance of various factors for their buyers (customers) in different countries. These scores were obtained from six firms selling to both China and the USA. The respondents were asked to rate the importance of four factors to their customers on a five point scale. The average scores are shown below in Fig. 1.

Fig. 1. U.S. and China Buyers' Requirements for B.C. Forest Products

Notes: 5 = very important; 1 = not important.

Source: Authors' interviews with representatives of B.C. forestry producers.

For buyers in China, as can be seen from Fig. 1, the most important factors are price and the ability to provide large volumes. For the U.S. buyers, quality and compliance with environmental standards are the two most important factors. There would seem, therefore, to be significant demand differences between the two markets with further analysis warranted of whether these differences result in changes in industry standards.

We analyze each part of the forest products sector but it should be noted that all three – lumber, pulp and paper, and other wood products such as panel boards – all come from the same resource: the tree. And any single tree can, and typically does, provide products for all three sectors. This is important to bear in mind in the analysis that follows.

3.2. Lumber

The lumber sector produces five main grades which, in descending order of quality are J-grade, Select, Number 2 and better, Number 3, and Economy. Each grade is approved by an industry standards authority and stamped accordingly. In terms of product standards, the highest grades have the lowest defect rates with respect to characteristics such as lumber straightness, warping, and knots. The growing and harvesting process is therefore the same for all grades of lumber as they can all be derived from the same tree. The grade differences arise in the milling process. The production process is designed to maximize the amount of the high grade lumber from a tree by a computerized production process which adjusts the cutting of each tree.

In general, the highest grade lumber is used in high-end construction/housing in Japan and the USA, the mid grades – for the construction/housing and retail sectors in the USA and the lowest end lumber – for construction in China. In the Chinese market much of the lumber is used in making forms for pouring concrete and, as such, requires only a lower quality product. This explains, in part, the observations above about customer requirements in the Chinese and U.S. markets, with Chinese buyers being more concerned with price than quality. From B.C. forest companies' perspective, this demand represents an important market for the large supply of pine beetle damaged wood being milled.

While this is a reasonable first approximation, it is noteworthy that the Chinese market has changed rapidly and an increasing amount of the somewhat higher grades of lumber are also being demanded for use in furniture production and in housing construction, for example, in door construction where wood stripping is replacing some concrete construction. This demand has arisen in part because of the efforts of the provincial government to change building codes in China (B.C. Ministry of Forests and Range 2002, and B.C. Ministry of Forests and Range/Canada Department of Natural Resources 2009). Changing process standards in construction in China is therefore changing product mix in lumber imports and this has benefitted B.C. exporters in both quantity and quality terms.

Even though the Chinese buyers are not as concerned with the process standards, for example, with respect to environmental stewardship; nevertheless, the products meet the same (high) process standards because all lumber grades come from the same tree and so the tree must be processed in a way that meets the standards set in the highest standards market. Forest certification has expanded significantly over the past two decades or more and has become a major influence on the forestry industry (see Cashore et al. 2004).

There are a number of competing and overlapping standards set by different certification organizations such as the International Organization for Standardization (ISO), Forest Stewardship Council (FSC), Sustainable Forestry Initiative (SFI), and Canadian Standards Association Sustainable Forest Management Standards (CSA), and the world's largest forest certification body, the Programme for the Endorsement of Forest (PEFC) certification, which endorses both SFI and CSA standards which are based on international criteria.6

For B.C. lumber firms, the two most relevant standards for their exports to the USA are the process standards required for Forest Stewardship Council (FSC) and the Programme for the Endorsement of Forest Certification (PEFC) approvals in order to sell in the USA. The major retailers, such as Home Depot, for example, require that lumber meets one or both of these certification standards. If these certification standards are to be met for one part of the tree, then they are met for all parts, regardless of the final export destination. However, B.C. lumber does not (typically) meet FSC standards because of on-going land claims involving First Nations in the province but does meet the PEFC standards and hence gains market acceptance. The U.S. environmental groups have brought pressure on the U.S. larger retails to ensure that their national and international suppliers responsibly harvest lumber. This has ensured that the PEFC compliant process standards, which B.C. exports to the USA must meet, also applies to their exports to China as well.

This is the general case. Many companies operate their mills as independent profit centres and for them the market diversification is an important strategy and so they prefer to sell to more than one market. In one instance, however, a large company has switched one mill to produce lumber exclusively for the China market with no production going to the USA. This decision was based on the low quality pine beetle damaged wood found in some timber supply areas in the central interior of the province of B.C.

There is some evidence that product standards have changed in the designated China only-mill. This arises because the lumber grades described above are particular to the North American market (although also used in Japan) but do not have global applicability. Furthermore, the grade standards set in North America are primarily concerned with the strength of the lumber and therefore its suitability for particular construction purposes.

The North American grading system does not correspond exactly with the appearance of the lumber, a factor which has more weight in other countries where lumber is used for many different purposes beyond the (housing) construction trade. As a result, the China-only mill has introduced variants of the North American grading system specifically for the Chinese market. This is not necessarily a lowering of product standards and might best be seen as an adaptation of standards to different market conditions, differences which are captured by the use of the term ‘custom lumber’ to describe this adaptation.

Nonetheless, there is also evidence that customers in China have adapted their product standards and are increasingly accepting North American length and width dimensions. Initially, one China-specific mill we analyzed had to change its product standards to meet Chinese customer preferences (as noted above, globally there are no standard industry product standards and different countries and regions have different board lengths and widths) but the latter then changed to accepting North American product standards as a way of obtaining increased volumes.

Because of the different uses of lumber in China, there are some changes in the production process and product standards. For example, lumber destined for China might not be kiln-dried or put through a planer mill meaning that its quality is lower than that sold to the North American market. Kiln-drying is part of the lumber production process designed to ensure that lumber has the technical strength characteristics required of building structures. Kiln-drying processes and the resulting kiln-dried lumber stamp are administered by the North American lumber industry itself. Since lumber destined for the China market is not used for building frame construction but mostly for pouring concrete then it does not need to be kiln-dried; to do so would be wasteful in this sense of meeting higher standards than are required for purpose. Instead, the lumber from the China-specific mill undergoes a heat treatment process designed to ensure that all insects are killed and the standards for which are set by international government agreements. Thus, product standards are lower but this better seen as standard adaptation based on different end usage than a lowering standards caused by a change of importing country.7

In general though, B.C. companies see their high process standards as a comparative advantage in selling to the Chinese market. As noted above, the Chinese buyers now include furniture manufacturers (although typically not directly but through a Chinese import agent). Since much of the furniture is for re-export to the USA it must meet the conditions of the 2008 Lacey Act in the USA which stipulates that all imported wood products must conform to (own country) regulations regarding legal sourcing.8 B.C. companies can prove this and this gives them a significant advantage over the Russian lumber (China's largest supplier) where illegal logging is prevalent. B.C. lumber is therefore preferred by the Chinese buyers and they are prepared to pay a premium for it over other supply sources which cannot provide legal harvesting certification. Thus, B.C. lumber exported to the USA but via a Chinese furniture manufacturer is again subject to process standards established in the USA.

3.3. Pulp and Paper

With respect to pulp and paper products, there are no independent industry product standards. The quality of pulp is determined by its tensile (or tear free run length) with companies monitoring this and pricing according to tensile strength. Company grading standards do exist although there is no industry-wide classification of grades. The quality of the pulp depends primarily on the quality of the wood chips used and the quality depends upon source of supply; wood chips in northern B.C. generally have high tensile strength, compared to European chips and the U.S. chips have even lower tensile strength.

Even so, pulp is used for different purposes in part depending on its quality and so the pulp and paper sector in B.C. produces three main products. These are publication quality paper (for magazines and newspapers), bulk consumer paper products (such as tissues and napkins) and specialty products (such as wallpaper, veneer board, fibre cement board and cigarette tips). The most profitable product type is publication paper followed by specialty products and then bulk consumer products (especially out-of-home products used in institutions, gas stations, restaurants, etc.). According to one of the province's major pulp and paper producers, there have been significant changes in its product mix over the past decade in part due to the impact of the internet on the publication industry. A decade ago, approximately 70 per cent of the product was in the form of publication materials, 15 per cent was bulk consumer products and 15 per cent was specialty products. Publication paper has now declined to 25 per cent and consumer and specialty products now represent 25 per cent and 50 per cent, respectively.

As well as the product composition changes, there have also been market shifts, as shown in Section 2, and each of the major export markets – the USA, Europe and China – which the company supplies has a different product mix. This is shown below in Table 6.

Table 6

One Firm's Paper Exports by Product Mix and Country (percent)

| Export market | Type of Pulp and Paper Product | ||

| Publication | Consumer | Specialty | |

| USA | 40 | 20 | 40 |

| China | 0 | 40 | 60 |

| Europe | 30 | 0 | 70 |

Source: Authors' interviews with one firm.

While there are significant differences in the product mix supplied to each of the major markets, production is still organized by product group rather than by end market. That is, pulp is not produced separately for each market, and not sourced from separate timber supply areas for each market, but subject to joint and integrated production. As a result, the process standards set in the highest standard export market are again the ones that set the standard for all export markets.

While there are no independent (or industry) product standards, there are independent process standards as set by the FSC and PEFC. PEFC standards are widely required for export to the USA, Europe and Japan and FSC is preferred in some cases. For example, major tissue manufacturers, such as Kimberley Clark, request FSC certified product if it is available and are willing to pay a premium for it; Proctor and Gamble does not require FSC certification but prefers it if it can be supplied at no additional cost. Consumer groups targeting these companies with campaigns such as Clearcut for Kleenex have pressured major tissue manufacturers into demanding compliance from their suppliers with some process standards certification. As noted above, forest products from B.C. do not typically meet FSC conditions but are PEFC compliant. Thus, while lower quality bulk consumer products may be exported to China, for example, the process standards followed are those set by the higher quality product destined for the U.S. market.

3.4. Other wood products

While wood chips are used in the production of pulp and paper products, they are also used in the production of medium density fibre (MDF) board, oriented-strand board (OSB) and in particle board, as well as a new product, bioenergy wood pellets.

One destination for wood left over from milling operations is particle board which has a variety of uses, with one of the main ones being for the production of household cabinets (mostly kitchen cabinets). Particle board is manufactured in B.C. with the traditional market being the USA. However, limited diversification into the China market has also taken place especially in the wake of the U.S. housing slump and there is also use in Canada. Canada has some regulations on process standards related to particle board and China has fewer, but the highest process standards are set by the California Area Resources Board (CARB). Any wood products sold in California must meet Environmentally Preferred Product (EPP) certification as well as process standards on formaldehyde levels and be stamped as compliant. The B.C. company producing the particle board has no certainty where its products end up; they could, for example, be used by a cabinet manufacturer in Vancouver which then exports to California. Or it could be used in a product which is then carried by a major retailer such as The Brick which also sells in California. So the company is 100 per cent CARB compliant, even though it is unsure how much of its product ends up in the California market, because it must meet the CARB standard in order to be able to enter into the selling chain and to protect itself against possible lawsuits. Again the highest standard jurisdiction sets the standard for all of the products because of integrated production.

This provides a literal example of the global ‘California effect’ (see Cashore et al. 2007: 159) where higher standards in one coveted market have driven up standards by other producers also wanting access to it. However, it should be noted that while these process standards should be applicable to all producers, the B.C. firm believed that it was facing a degree of unfair competition because other firms, especially from China, did not adhere to the regulations. The reduction in inspections as a result of the California fiscal crisis as well as the difficulty of prosecuting Chinese firms put the latter in a better market position. This reinforces a point that the regulations described in Fig.1 above require enforcement to be effective.

4. Concluding Reflections

China's economic rise has implications for resource use and global trade on many levels. Here, we have focused one important but neglected issue, namely, whether increasing north-south trade in commodities will affect product and process standards in the north and have examined this in the specific case of forest product exports from B.C. to China. Based upon the analysis above, we conclude that product and process standards have not been affected to date by the industry's rapidly expanding trade with China. This result arises from the fact that integrated production technology and fibre source results in forest sector products which are exported to markets in both the north and south. Therefore, the standards which are required in the highest standard export market set the minimum standard for the product destined for all export markets. B.C. forest product firms comply with government set standards such as the mandatory 2008 U.S. Lacey Act and California Area Resource Board and the voluntary civil society certifications such as the Program for the Endorsement of Forest Certification in order to ensure access to the U.S. market. This has not only meant that process standards demanded by international civil society organizations for export to the USA are also applied for export to China but also that these and governmental regulatory standards have actually been seen as a competitive advantage when exporting to China as products may then be re-exported back to northern markets.

At a time when China first emerged, a major economic actor on the global level, Freeman (1995) asked whether the lower wages in China would push down wages elsewhere in a provocatively entitled article Are your wages set in Beijing? His answer was ‘No’. In analyzing China's emergence as a major export destination for a northern product, we reach the same answer to the question of whether Canadian and northern international environmental standards, as an example of a northern country's standards, are set in Beijing. Our discussion also demonstrates that standards set by governments and non-state actors can both play a role, as the Lacey Act and PEFC standards show. As such they should be seen as complementary rather than alternative standard setting strategies (see also Cashore et al. 2007 on this point).

The perhaps reassuring conclusion for northern countries that their standards are not set in Beijing is subject to a caveats, if a ‘tipping point’ is reached in trade with China and producers find it more profitable to specialize in production for the China market. That is, the longer term impact of China's preference for lower grade forest products and lesser concern with process standards depends, in large part, on how large China's market becomes for B.C. forest products. At present the integrated production for all export markets provides an effective check on standards intensity but it is possible to conceive of a situation where a tipping point is reached where the China market becomes so much more important than other export markets (including the USA) that the requirements of the China market will more likely dominate.

Our assessment is that such a ‘tipping point’ is unlikely, notwithstanding the greater global role of the China market. While China's market for lumber is likely to grow (Sun and Canby 2010) it is still unlikely that the growth of the China market for B.C. forest products will grow at anything like the same rate as it did in the 2000s. This has more to do with what is likely to happen to demand in the USA than in China. Many B.C. industry actors believe that the industry is poised for a ‘super cycle’. This describes the situation in which demand is maintained from China but demand from the USA increases as the U.S. housing market starts to rebound from the sub-prime crisis. As one interviewee stated ‘before 2006 there was no China, then until 2012 there was no USA. In the future we will have both’. This will mean that the Chinese market will remain significant as producers seek to continue diversification away from reliance on the U.S. market but the latter will remain a core market given its proximity and preference for higher quality (and hence higher priced) product. This means that a further shift towards China is unlikely given the increased demand from the USA and the greater price sensitivity of the Chinese export market.

The combined effect of the demand changes outlined above for the B.C. forest products sector is that the major part of its ‘China shift’, shown in Tables 1 to 3, probably, has already occurred; indeed, the 2012 data already show the U.S. market share rebounding. As long as the export market remains diversified – including the high-standard U.S. market – and as long as integrated production continues – so that the company does not know where the tree is going when it enters the mill – then under these conditions, the new patterns of natural resource trade that have occurred will have little noticeable impact on standards.

As a final point, however, it should be noted that while further shifts towards the China market may not be expected, there is a difference in the composition of forest products exported to China versus the USA. We noted above how product standards tended to be lower in lumber exports to China since they had different end uses than in the USA. In addition, and more seriously from an economic development point of view, raw log exports from B.C. have also increased significantly to China.9 This can be seen as a ‘re-primarization’ challenge to Canada but, since raw log exports require provincial government approval, this has more to do with domestic political economy considerations than international markets alone. We have therefore focused here on trade shifts and process standards but there are other issues associated with increased trade with China that should be of concern to Northern governments.

In terms of the process standards which have been the main focus of this paper, the implications for civil society and governments are that high standards in core markets can and do have important repercussions for global standards. With integrated production, it is the standards set in California which determined those followed for B.C.

The main conclusion is that high standards, both voluntary and mandatory standards continue to effectively influence production decisions of firms in northern countries despite increased trade with southern countries with lower standards. Therefore, both civil society organizations and governments should be aware that standard setting and enforcement remain important tools to promote labor and environmental standards.

Acknowledgment

We thank Ethan Anderson and Ryan Lidder for their research assistance and the Social Sciences and Humanities Research Council of Canada for funding.

NOTES

1 Of course, many developing countries consider this an attempt to limit their exports.

2 The study complements the primarily quantitative work on the impacts of standards on the volume of trade (for a useful review, see Swann 2010). These studies are primarily focused on how changes in standards affect trade; we analyze here a reverse issue of how changes in the direction of trade affect standards.

3 In 2012, British Columbia accounted for 30 per cent of Canada's exports to China, 41 per cent of exports to Japan and 52 per cent of exports to South Korea. B.C. accounted for 60 per cent of Canada's forest exports in that year. URL: http://www.bcstats.gov.bc.ca/StatisticsBySubject/Exports Imports/Data.aspx.

4 Pacific Rim countries are: Japan, Hong Kong, Malaysia, Brunei Darussalam, Singapore, Laos, Mongolia, China, Indonesia, North Korea, South Korea, Philippines, Macau, Taiwan, Thailand, Vietnam, Australia, Fiji, and New Zealand. URL: http http://www.bcstats.gov.bc.ca/StatisticsBySubject/Exports Imports.aspx.

5 As a first examination of the issue, we concentrate here on the major firms in the forest sector. Subsequent research on whether the conclusions reached here also hold for smaller industry players may be warranted.

6 For an example of how one major forest company producing in B.C. states that it meets these standards see http://www.canfor.com/responsibility/environmental/certification.

7 This can, however, be seen as more general trend towards the export of lower value-added products to China, a point to which we briefly return in the concluding section.

8 For details see http://www.eia-global.org/lacey/P6.EIA.LaceyReport.pdf.

9 B.C. raw log exports to China increased approximately ten-fold between 2007 and 2011 to over $300 million. URL: http://www.bcstats.gov.bc.ca/StatisticsBySubject/ExportsImports/Data.aspx.

References

B.C. Ministry of Forests and Range. 2002. China Trade Mission to Expand B.C. Forest Products Market. Media release, November 12. URL: http://www.for.gov.bc.ca/ pab/media/dejong/2002/11/12/. Accessed June 19, 2013.

B.C. Ministry of Forests and Range / Canada Department of Natural Resources. 2009. ‘Shanghai Code Approval Opens Up Market for Canadian Wood’, Press Release, November 9. URL: http://www2.news.gov.bc.ca/news_releases_2009-2013/2009FOR0072-00 0595.htm. Accessed June 19, 2012.

Barry, C., and Reddy, S. 2008. International Trade and Labor Standards: A Proposal for Linkage. New York: Columbia University Press.

Borras, Jr. S. M., McMichael, P., and Scoones, I. 2010. The Politics of Biofuels, Land and Agrarian Change: Editors' Introduction. The Journal of Peasant Studies 37(4): 575–592.

Busse, M. 2004. Trade, Environmental Regulations and the WTO – New Empirical Evidence. Journal of World Trade 38(2): 285–306.

Cashore, B., Auld, G., Bernstein, S., and McDermott, C. 2007. Can Non-State Governance ‘Ratchet Up’ Global Environmental Standards: Lessons from the Forest Sector. Review of European Community and International Environmental Law 16(2): 158–172.

Cashore, B., Auld, G., and Newsom, D. 2004. Governing Through Markets: Forest Certification and the Emergence of Non-State Authority. New Haven, NJ: Yale University Press.

Cypher, J. M. 2007. Back to the 19th Century? The Current Commodities Boom and the Primarization Process in Latin America. In LASA XXVII International Congress Session ECO20, Montreal, Canada, September (pp. 5–8).

Freeman, R. 1995. Are Your Wages Set in Beijing? Journal of Economic Perspectives 9(3): 15–32.

Grinin, L. 2011. Chinese Joker in the World Pack. Journal of Globalization Studies 2(2): 7–24.

Henderson, J. 2008. China and Global Development: Towards a Global-Asian Era? Contemporary Politics 14(4): 375–392.

Jenkins, R., Peters, E., and Moreira, M. 2008. The Impact of China on Latin America and the Caribbean. World Development 36(3): 235–253.

Kaplinsky, R. (ed.) 2005. Asian Drivers: Opportunities and Threats. IDS Bulletin 37(1).

Kaplinsky, R., and Farooki, M. 2010. What Are the Implications for Global Value Chains? When the Market Shifts from the North to the South? World Bank, Poverty Reduction and Economic Management Network, International Trade Department. Policy Research Working Paper 5205, February.

Kaplinsky, R., and Morris, M. 2009. Chinese FDI in Sub-Saharan Africa; Engaging with Large Dragons. European Journal of Development Research 21: 551–569.

Kaplinsky, R., Terheggen, A., and Tijaja, J. 2011. China as a Final Market: The Gabon Timber and Thai Cassava Value Chains. World Development 39(7): 1177–1190.

McDermott, C. 2012. Trust, Legitimacy and Power in Forest Certification: A Case Study of the FSC in British Columbia. Geoforum 43(3): 634–644.

Parfitt, B. 2010. Axed: A Decade of Cuts to BC's Forest Service / Canadian Centre of Policy Alternatives, December.

Peebles, F. 2012. Mills Look Abroad for Lumber Sales. Prince George Citizen, July 20.

Rehn, C. 2013. China Named World's Biggest Net Importer of Oil, Overtaking USA. Energy Global, posted 11 September. URL: http://www.energyglobal.com/news/exploration/articles/China_named_world’s_biggest_net_importer_of_oil_overtaking_USA.aspx. Acces-sed November 25, 2013.

Roache, S. 2012. China's Impact on World Commodity Markets. IMF Working Paper, May.

Scott, D. 2007. The 21st Century as Whose Century? Journal of World Systems Research 13(2): 96–118.

Spence, M. 2011. The Next Convergence: The Future of Growth in a Multi-Speed World. New York: Farrar, Straus and Giroux.

Sun, X., and Canby, K. 2010. China: Overview of Forest Governance. Markets and Trade. Washington: Forest Trends.

Swann, G. P. 2010. International Standards and Trade: A Review of the Empirical Literature. OECD Trade Policy Working Papers 97. OECD Publishing.

UNCTAD. 2013. Trade and Development Report. Geneva: UNCTAD.

U.S. International Trade Commission. 2006. The Effects of Increasing Chinese Demand on Global Commodity Markets. Staff Research Study 28, Publication 3864, June.

World Trade Organization. 2013. WTO, International Trade Statistics, 2013. Geneva: WTO.

Размещено в разделах