Globalization and the Performance of Commercial Banks in Nigeria

скачать Автор: Ekong, Uduak Michael - подписаться на статьи автора

Журнал: Journal of Globalization Studies. Volume 7, Number 1 / May 2016 - подписаться на статьи журнала

The present study empirically investigates the effect of globalization on com-mercial banks performance in Nigeria in the period from 1980 to 2013 using Error Correction Mechanism (ECM). This has been motivated by the ob-served falling financial assistance to the economy by commercial banks even in the face of growing global participation. The result shows that a positive effect of globalization on improving performance of commercial banks in Ni-geria will only occur at the price of time. Stated specifically, a percentage increase in participation in globalization will improve Nigerian commercial banks' ability to extend credit to the private sector by 10 percentage points and above as time passes. The study recommends improvement in local con-tent policies in prioritized sectors of the economy to shorten the time-cost and reverse the trend.

Keywords: globalization, commercial bank performance, economic performance, credit assistance, Nigeria.

Introduction

Early thoughts of globalization were that when the world large disintegrated economic units are integrated together to form a more closed circuit economic unit, the gains can be derived from speed, closeness and unity of regions. For many, such nexus is created through trade and capital flows. Economic theory suggests several ways in which globalization can spur performance of some sectors or even different sectors in another economy. For instance, international trade is believed to allow for greater specialization and division of labour, resulting in increased productivity and output. If both labour and output or even other specialties, are circulated among regions, performance could be enhanced in surrounding regions. Intensified competition arising from trade liberalization may also spur innovations and performance as firms try to increase their market share and operations. This made Ozughalu and Ajayi (2007) to assert that globalization has paved the way for increasing harmonization of the economic rules that govern relationship between sovereign nations, establishment of structures that support and facilitate dependence and interconnection and creation of global market place. The importance placed on globalization particularly by the developing economies of the world is that very little or even nothing could be achieved without the support of other countries. Ajayi and Atanda (2012) noted that with the increasing wave of globalization, distance has ceased to be a major barrier in communication and other various forms of transactions.

Although it has been argued that globalization enhances increased opportunities for countries to accelerate their economic growth and development potentials, the outcome has often been the uneven spread of growth across regions. At some instance, the worst hit of the disparity in spread of economic benefit of globalization are the developing economies like Nigeria. The factor accounting for such disparity is the differences in resource endowment and location of a country that may hinder its integration into the global market. Thus, this probability exists for many countries to face.

Given the foregoing, it is necessary to examine the performance of commercial banks in Nigeria to determine which side of the coin they belong. Banks perform a lot of statutory work to deepen a country's financial system or promote economic growth and development. Commercial bank performance is the accomplishment of a given bank function measured against preset banking standard of service delivery. Bank performance is deemed to be the fulfillment of financial rules and obligation of delivering value returns on shareholders wealth on the one hand and servicing the financial needs of the entire economy on the other, in a manner that releases the bank(s) from all liabilities. More generally, this is often done by performing two kinds of functions – micro-functions and macro-functions.

The micro-functions include but are not limited to collection of deposit, credit extensions, receiving interest, creation of medium of exchange, issuing of cheque, circulation of money; whereas in the macro-functions the activities like capital formation, contribution to economic development, transmission of money, and support of the industrial development may be considered. The combination of these two broad functions is taken into account when analyzing the bank performance around the world.

Over the years in Nigeria, economic literature pays a great deal of attention to globalization and economy with little or no emphasis on the performance of commercial banks in credit allocation. This is where this exercise finds a place in the literature.

2. Literature Review

2.1. Theoretical Issues

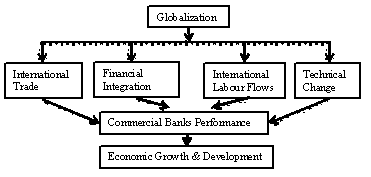

There are growing concerns that globalization affects economic growth and development and by extension the performances of some sectors of the economy like the banking system. In fact, the core of financial globalization and financial integration is achieved through the banking system of which the commercial banks are the pivot. According to Nwokoma (2004), a simple nexus of globalization and the economy can be represented as follows (Fig. 1).

|

Fig. 1.

Source: Adopted and modified from Nwokoma 2004.

It is interesting to note that payment flows from other facets of globalization are facilitated by the performance of the Commercial banking system to influences growth and development. Confirming this position, UNCTAD 2003 asserts that globalization process has turned the financial world environment into the one which steadily allows indigenes to make cross border investment with little restrictions and equally allowing entities from other countries to invest in the domestic economy of other countries and transfer the proceeds without restrictions. This ultimately affects growth as shown in Fig. 1 above.

Given the perceived influence of globalization, many scholars and research institutions have attempted a quantitative measure of dynamics of globalization. The Globalisation Index by Centre for the Study of Globalisation and Regionalisation (CSGR) and the Konjunkturforschungsstelle (KOF) Index of Globalization both measure how globalized a country is basing on economic, social, and political measurements. The A. T. Kearney study also considers these factors but adds technology as a criterion to identify which countries are globalizing and which ones are not. This method is useful for determining a country's ranking but is otherwise limited, as it does not take into account the way the policy decisions are impacted by globalization and vice versa. While some indices provide a comprehensive review of one aspect (which is the case with the Torben Andersen and Tryggvi Thor Herbertsson index), it limits the measurement of globalization to one sector, therefore rendering it only partially valid, as multiple factors contribute to the development of state policy. Finally, the Randy Kluver and Wayne Fu Index looks at the phenomenon of cultural globalization. Again, by limiting the scope of measurement, one cannot gauge a clear picture of a policy position at any given time on any given issue (Al-Rodhan, Stoudmann, and Herd 2006). More recently, the Geneva Centre for Security Policy (GCPS) has proposed a measure of globalization that considers the impact and responses from surrounding regions just to account for stability in the global economy.

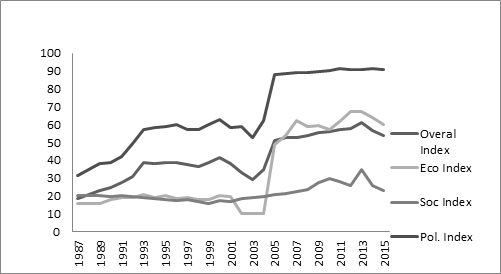

Fig. 2 provides the globalization index for Nigeria for the period from 1987 to 2015. As shown in Fig. 2, political globalization flourished significantly over the years. Not minding the political challenges the country have experienced during the period. Economic globalization has suffered most of the shocks particularly between 2001 and 2004 when the country was adjusting to early years of economic democratization, forcing the overall index to decline. As the index shows, social globalization is not given adequate attention in Nigeria. Fig. 2 also shows that the periods leading to elections reduce global participation in general activities in the country as all the indices have fallen in years following 2013 except the political one itself. How well these influences affect the performance of commercial banks in Nigeria will be shown.

Fig. 2. Nigeria's growth in globalization, 1987–2015

Source: the author's studies.

2.2. Globalization and Commercial Banks Performance

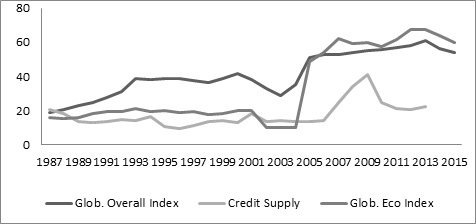

Fig. 3 shows the percentage growth of globalization and credit allocation by the commercial banking system in the period from 1987 to 2015. The figure reveals interesting points concerning the globalization / commercial banks performance nexus. Commercial banks performed poorly in credit allocation between 1987 and 2014. Beginning from 1987, credit allocation by commercial banks in the globalized era declined from 20.8 per cent to 13.2 per cent in 1990, whereas globalization grows from 18.7 per cent to 24.7 per cent in the same period. From 1991 credit allocation grew from 13.5 per cent to 16.8 per cent in 1994, and fell gradually to a single digit of 9.6 per cent in 1996. The trend of growth in credit allocation by commercial banks to the economy only witnessed a progressive growth from 13.4 per cent in 2004 to an all-time peak of 41.3 per cent in 2009, before falling sharply to 22.3 per cent in 2013.

Fig. 3. Nigeria: Globalization and Commercial Bank Performance

Source: the author's studies.

Within the period under review, globalization grows extensively over and above commercial banks performance. Thus, commercial banks performance lagged behind globalization in development process. This is attributed in part to weakening economic globalization for most of the years. Economic globalization fell from 20.2 per cent in 2000 to an all-time low value of 10.1 per cent in 2004. Economic globalization retarded commercial banks performance in credit assistance to the real economy so much so that real growth of the economy fell from 5.3 per cent in 2000 to as low as 3.8 per cent in 2003.

2.3. Empirical Relationship between Globalization and Commercial Banks Performance in Nigeria

As pointed out earlier, many studies have paid attention to the effect of globalization on the growth of economies in the world, (e.g., Verter and Osakwe 2015; Uma and Obidike 2013; Ajayi and Atanda 2012; Adams 2010) with little or no recourse to how commercial banks may be affected. However, there are traces of the effect of globalization on commercial banks performance.

In their study, Lozane-Vivas, Pastor, and Pastor (2002) examine the performance of a sample of banks in ten European countries, and conclude that country-specific environmental conditions exert a significant influence on the performance of each country's banking industry than globalization. Ajilore (2005) applied co-integration and associated error correction procedure on quarterly data in Nigeria from 1986 to 2000 and found that the surge in foreign private capital inflow that occasioned the opening of the country's capital account had positively impacted on the growth performance in Nigeria.

Goyal (2006) carried out a study on the impact of globalization on developing countries with special reference to India. He discovered that globalization in India had a favourable impact on the banking industry and overall growth rate of the economy. The growth rate was as low as 3 per cent in 1970, but almost doubled to 5.9 per cent in the eighties as a result of globalization. Ogunleye (2008) notes that if such liberalization allows for external influences, a long run relationship could be established in economic growth, output volatility, and consumption volatility.

Adegbite and Adetiloye (2013) investigated the relationship between financial globalization and domestic private investment with Nigeria on the focus. In their study both descriptive and econometric analyses were employed over the data for the period from 1970 to 2007. Their result shows that financial globalization effect was marginal in the economy. They recommend a greater need for autonomous investment to crowd in other investments by implementing policies that encourage investment in the economy, pointing out that the situation may not improve until there is a proactive and deliberate action from the government to improve investment, especially of infrastructure, in the economy.

Osamor, Akinlabi, and Osamor (2013) applied panel regression on panel data from Nigerian commercial banks from 2005 to 2010 to examine their performance. The period conforms to the banking sector reforms of consolidation and further liberalization of the sector. The study reveals that foreign private investment, foreign trade and exchange rate positively and significantly affected the profit after tax of Nigerian commercial banks, but the magnitude of such effect was indeterminable due to variations on data for performance measure of the banks under study.

Using the primary data set, Mamman and Baydoun (n.d.) examine the meaning of globalization in Nigeria and how it affects the managers of banks in the conduct of business. The study was carried out using a sample of 204 professionals and managers from a commercial bank. The sample included directors (2 per cent), senior managers (9.3 per cent) and middle managers (54.9 per cent), as well as professionals, namely, accountants and lawyers (33.8 per cent). Respondents were asked to indicate the extent of their agreement to the statements designed to investigate the meaning of globalization from their own point of view as the Nigerians. The study found out that a majority (60.3 per cent) did not view globalization as free movement of labour. This means they consider globalization as restricted with respect to the movement of capital and goods, while a significant minority (27.4 per cent) believes in free movement of labour. What is very clear and emphatic from the study is that the sample sees globalization symbolizing the integration of Nigeria into the international economy in the order (89.2 per cent). There is also some evidence that a significant number (48.5 per cent) believe that globalization has selfish connotations. Overall, it appears globalization benefit the managers after reforms.

3. Methodology

The present study adopts a modified version of Adegbite and Adetiloye (2013) model of financial globalization and domestic investment specified as:

CR*t = F(TOPt, ODAt, EXCRt, INFLt, RGDPt, Globt , RRt ) (1)

where CR*t is the ratio of Credit Supply to Private Sector to GDP used to captured credit availability to the Nigerian economy and hence the Performance of Commercial Banks; TOPt is the index of trade openness proxied by the ratio of imports plus exports to nominal GDP. Trade openness is a measure of the degree to which the banking system is able to intermediate funds across borders through their trade and investment decisions. Some studies have been tempted to use this as a proxy of globalization (e.g., Uma and Obidike 2013); ODAt is an index of Official Development Assistance to the country measured by the growth rate of ODA ; EXCRt is exchange rate, and gauges the price of cross border globalization in Nigeria; RR is real interest rate and captures the price of benefiting from Commercial Banks Performance in the globalized period by the private economy; Globt is globalization index and captures the policies pre- and post- globalization effect in Nigeria such as SAP; €I is error term.

Transforming Equation (1) into an Error Correction Model yields

ΔCR*t = θ0 + θ1ΔGDUMt + θ2i ƩΔCRt-i + θ3iƩΔGDUMt-i + θ4 ECMt-1 + € (2)

where Δ indicates the first difference of the series; θs are the parameters to be estimated; i is the number of lags included in the difference of both the dependent and the independent variables; ECMt-1 is the lagged error term; GDUM is all the explanatory variables in the system; t is time period; and € is white noise error term.

Our prediagnostic test of unit root followed the augmented dickey fuller, specified as

∆y = α + η yt-1 + λ ∆yt-1 + ep (3)

where y denotes the variable of interest. Under the null hypothesis that H0 : η = 0, against the alternative H1 : η < 0, at 5 per cent level of significance, it was decided that our variables follow a steady AR process. A Johansen co-integration test was used to establish the trend relationship.

The data for the study was sourced from CBN statistical bulletin (various issues), World Bank country data for Nigeria and KOF index of globalization for Nigeria.

4. Analysis of the Effect of Globalization on Credit Allocation to the Economy by the Commercial Banks in Nigeria

Our model selection criterion is presented in Table 1. Here, the linear specification of the relationship reveals an interesting and significant relationship between the variables and has been selected for the analysis.

Table 1

Long Run Estimation of Model Three Using Different Functional Forms

Dependent Variable CR*

| Variables | Linear | Double Log | Semi-Log | Exponential |

| Constant | 24.2557*** (6.1569) | –0.623223 (–0.6366) | –39.9359 (–1.9742) | 2.9988*** (12.5569) |

| TOPt | –0.148992** (–2.2886) | –0.270815 (–1.2626) | –4.79811 (–1.2092) | –0.565212 (–1.3717) |

| ODAt | –0.0052686** (–2.4326) | –0.02149 (–0.3830) | 0.0532046 (0.0536) | –3.92023** (–2.1301) |

| EXCRt | 0.0626229** (2.1722) | –0.35520** (–2.6742) | –5.38999** (–2.7213) | 0.00102 (0.7347) |

| INFLt | –0.379041 (–1.6185) | –0.00474 (–0.0260) | –1.01723 (–0.3211) | –0.01811 (–1.4040) |

| RGDPt | –0.437663*** (–4.8276) | 0.304857*** (3.1373) | 4.72458*** (3.0787) | 1.61208** (2.1155) |

| Globt | 10.0721*** (2.9871) | 0.547531 (1.2543) | 7.64003 (1.0804) | 0.566397** (2.6294) |

Table 1 continued

| RRt | –0.393744 (–1.7483) | 0.00835 (0.0549) | 1.00031 (0.3660) | –0.018597 (–1.5045) |

| R2 | 0.3834 | 0.4120 | 0.3483 | 0.4739 |

| Adjusted R2 | 0.2601 | 0.2945 | 0.2180 | 0.35006 |

| AIC | 285.7688 | 41.57858 | 288.1475 | 38.80222 |

| SIC | 299.8584 | 55.66818 | 302.2371 | 54.65302 |

| P-value(F) | 0.000050 | 0.011532 | 0.112395 | 0.000000 |

| DW | 0.849025 | 0.702372 | 0.760436 | 0.750806 |

| Hannan-Quinn | 290.9646 | 46.77439 | 293.3433 | 44.64750 |

Note: ***, ** represents significance at 1 and 5 per cent respectively. Figures in brackets are t-ratios.

Source: author's study.

The results of the Unit Root test and the order of integration of the variables are presented in Table 2.

Table 2

Unit Root Test

| Variables | ADF at level | ADF at 1st diff. | Mckinnon Critical Value (5 %) | P-value | Order of Integration |

| RGDPt | –2.569221 | –5.056360 | –3.610453 | 0.0002 | 1(1) |

| ODAt | –3.558139 | –7.289303 | –3.605593 | 0.0000 | 1(1) |

| EXCRt | 0.437106 | –5.548944 | –3.600987 | 0.0000 | 1(1) |

| CRt* | –2.228267 | –5.303520 | –3.610453 | 0.0002 | 1(1) |

| INFLt | –3.417152 | –6.340955 | –3.605593 | 0.0000 | 1(1) |

| RRt | –3.603298 |

| –3.596616 | 0.0098 | 1(0) |

| Globt | –1.284832 | –6.403124 | –3.600987 | 0.0000 | 1(1) |

| TOPt | –1.912303 | –6.060719 | –3.600987 | 0.0000 | 1(1) |

Note: ** indicates significance at 10 per cent.

Source: author's calculations.

The results presented in Table 2 show that all the variables are non-stationary at level form except for Real Interest rate since their ADF values are less than the critical values at 5 per cent (for which the study adopt). The null hypothesis of unit root was accepted for all the variables at level (except for Real Interest rate (RR) which was stationary at level) but was rejected at 1st difference and rather accepts the alternative hypothesis that the variables are all stationary. Thus, we conclude that the variables under investigation are integrated of order one (i.e. I (1)) except for Real Interest rate (RR) which was 1 (0)). Since the variables are integrated, we therefore, examine the co-integrating relationship of the variables using Johansen co-integration procedure. The result is presented in Table 3.

Table 3

Johansen Co-integration Test Result between CRt*, TOPt, ODAt , EXCRt , INFLt , RGDPt , Globt , and RRt

| Hyp. No of CE(s) | Eigen value | Trace Statistics | 0.05 Critical Value | Max-Eigen Statistic | 0.005 Critical Value |

| None * | 0.796474 | 216.424* | 159.5297 | 65.27047 * | 52.36261 |

| At most 1* | 0.742011 | 151.1543* | 125.6154 | 55.54838* | 46.23142 |

| At most 2* | 0.657660 | 95.60595 | 95.75366 | 43.94995 * | 40.07757 |

| At most 3 | 0.464896 | 51.65599 | 69.81889 | 25.63707 | 33.87687 |

| At most 4 | 0.251651 | 26.01893 | 47.85613 | 11.88529 | 27.58434 |

| At most 5 | 0.213341 | 14.13363 | 29.79707 | 9.838393 | 21.13162 |

| At most 6 | 0.097959 | 4.295241 | 15.49471 | 4.226930 | 14.26460 |

| At most 7 | 0.001665 | 0.068311 | 3.841466 | 0.068311 | 3.841466 |

Note: * denotes rejection of the hypothesis at the 0.05 level. Trace test indicates the presence of two co-integrating equations and Max-Eigen value indicates the existence of three co-integrating equations at 0.05 level.

Source: the author's studies.

From Table 3 the trace test statistic indicates the existence of at least two co-integrating equations, while the Max-Eigen test statistic indicates the presence of at least three co-integrating equations both at five-percent level of significance which implies that there may be lasting co-integration of globalization and the ability of Commercial Banks in Nigeria to extend credit facilities to the economy. It will further show the effectiveness of the Nigerian banking system to key into International Financial Inclusion currently being popularized in some quotas. Thus, we reject the hypothesis of absent co-integration and proceed with the investigation of the co-integrating relationships. The result of the over-parametized model of commercial banks' credit performance to the economy and globalization is presented in Table 4.

Table 4

Over-Parametized Model of Commercial Banks Performance and Globalization

Dependent Variable: ΔCR*

| Coefficient | Std. Error | T-ratio | P-value | ||

| Const | 2.81612*** | 0.6720 | 4.1907 | 0.00106 | |

| ΔTOPt | –0.0422 | 0.0769 | –0.5485 | 0.59262 | |

| ΔTOPt_1 | –0.2314** | 0.0991 | –2.3349 | 0.03623 | |

| ΔTOPt_2 | –0.0093 | 0.0991 | –0.0940 | 0.92655 | |

| ΔODAt | –0.0060*** | 0.0019 | –3.1602 | 0.00752 | |

| ΔODAt_1 | –0.0024 | 0.0023 | –1.0581 | 0.30930 | |

| ΔODAt_2 | –0.00224 | 0.0022 | –1.0186 | 0.32699 |

Table 4 continued

| Coefficient | Std. Error | T-ratio | P-value | ||||||

| ΔlogEXCRt | –2.1558 | 1.4915 | –1.4453 | 0.17203 | |||||

| ΔlogEXCRt_1 | 2.54782 | 1.7509 | 1.4552 | 0.16934 | |||||

| ΔlogEXCRt_2 | –7.3337*** | 1.7159 | –4.2740 | 0.00091 | |||||

| ΔINFLt | –0.3927** | 0.1773 | –2.2149 | 0.04524 | |||||

| ΔINFLt_1 | –0.2921 | 0.1884 | –1.5506 | 0.14500 | |||||

| ΔINFLt_2 | 0.0744* | 0.0365 | 2.0358 | 0.06268 | |||||

| ΔRGDPt | 0.0145 | 0.2290 | 0.0632 | 0.95059 | |||||

| ΔRGDPt_1 | 0.0433 | 0.2283 | 0.1894 | 0.85269 | |||||

| ΔRGDPt_2 | 0.03473 | 0.1819 | 0.1910 | 0.85151 | |||||

| ΔGlobt | –6.1042** | 2.5929 | –2.3542 | 0.03495 | |||||

| ΔGlobt_1 | 1.48522 | 2.7640 | 0.5374 | 0.60010 | |||||

| ΔGlobt_2 | 8.40934** | 3.8689 | 2.1736 | 0.04881 | |||||

| RRt | –0.3991** | 0.1588 | –2.5133 | 0.02593 | |||||

| RRt_1 | 0.16963 | 0.1401 | 1.2109 | 0.24750 | |||||

| RRt_2 | 0.322134 | 0.1881 | 1.7129 | 0.11047 | |||||

| ΔCRt* | 0.06669 | 0.1366 | 0.4883 | 0.63349 | |||||

| ΔCRt*_1 | –0.2651* | 0.1230 | –2.1543 | 0.05056 | |||||

| ΔCRt*_2 | –0.7879*** | 0.2267 | –3.4750 | 0.00411 | |||||

| ECM_1 | –0.0072 | 0.1197 | –0.0602 | 0.95295 | |||||

| Mean dependent var | 0.312821 | S.D. dependent var | 4.593365 | ||||||

| Sum squared resid | 218.7745 | S.E. of regression | 4.102293 | ||||||

| R-squared | 0.727133 | Adjusted R-squared | 0.202389 | ||||||

| Log-likelihood | –88.96596 | Akaike criterion | 229.9319 | ||||||

| Schwarz criterion | 273.1845 | Hannan-Quinn | 245.4506 | ||||||

| Rho | –0.002698 | Durbin's Watson | –0.030823 | ||||||

Note: *, **, *** indicates significance at 10, 5, and 1 per cent respectively.

Source: the author's studies.

It is seen from the table that trade openness, official development assistance, inflation, real interest rate, credit supply to private sector, exchange rate and globalization were all significant at both current and various lagged levels.

Trade openness was negative in attracting foreign income to Nigeria's commercial banks for onward lending to the economy and also to stabilize their profit position in the current period to the tune of almost 4 per cent from every100 per cent trade financed. Such effect will be significant as time passes. The coefficient of ODA was negative for all the period but highly significant in the current period. This implies that ODA is not an important factor in commercial banks' lending portfolio. Unclaimed ODA may not have been extended to service production even at short term bases or may have been used to service investment that does not have real benefit in the economy. However, inflation will be negative and significant in the current time period but positive and significant after a time lag. This means that inflation will reduce foreign financial inflows to the commercial banking system as time passes and will eventually reduce the ability of commercial banks in extending credit facilities to the economy and, together with the insignificant real GDP and significant but negative real interest rate, present a harsh macroeconomic environment in pooling foreign financial resources into our economy. Perhaps, such macroeconomic environment combined makes it initially difficult for commercial banks and the economy in general to perceive the real effect of globalization. The pattern of globalization policies in the model proves this fact. From the dummy of financial globalization in the current period, we infer that globalization will not produce any useful effect to commercial banks credit allocation to the economy immediately. In fact because of such overall effect, even what was extended in the past periods cannot support the economy very well (as shown by the negative significant coefficients of the CR* lagged). The pooled foreign financial resources were not enough to extend financial assistance to the economy in the past, nor will that positively affect the current period. However, as the economy grows and adjusts, the positive and significant effect of globalization policies may become evident. This is supported by the globalization dummy index of 8.4 in lagged two periods.

The parsimonious short run dynamic model of the effect of financial globalization on commercial banks credit allocation to the economy is presented in Table 5. It shows that only trade openness in lagged one period, ODA in current and lagged one period, index of globalization policies in current period, inflation in current and one period lagged, credit supply to the economy in lagged one and two periods and exchange rate in current period, negatively affect credit allocation by commercial banks in Nigeria. The effect of real price of fund was mixed, negative at inception but positive afterwards. Contrary to expectation, real GDP was not found to be a determinant of Commercial Banks Credit Allocation in the period of financial globalization. The index of globalization policies was negative and significant in one per cent in current period. This means that financial globalization did not help commercial banks in Nigeria to extend credit to the private sector at the initial instance, but may do so after some time to the tune of over 9.2 per cent.

Table 5

Short Run Dynamic Model of Commercial Banks Performance and Globalization

Dependent Variable: ΔCR*

|

Table 5 continued

| ΔCR*t_1 | –0.2042*** | 0.0701 | –2.9117 | 0.00785 | ||||

| ΔCR*t_2 | –0.7645*** | 0.1983 | –3.8563 | 0.00080 | ||||

| ECM_1 | –0.4877*** | 0.1230 | –3.9655 | 0.00076 | ||||

| Mean dependent var | 0.312821 | S.D. dependent var | 4.593365 | |||||

| Sum squared resid | 241.0590 | S.E. of regression | 3.237410 | |||||

| R-squared | 0.699339 | Adjusted R-squared | 0.503255 | |||||

| Log-likelihood | –90.85746 | Akaike criterion | 213.7149 | |||||

| Schwarz criterion | 240.3319 | Hannan-Quinn | 223.2649 | |||||

| Rho | –0.090879 | Durbin-Watson | 2.012054 | |||||

Note: **, *** indicates significance at 5, and 1 per cent respectively.

Source: the author's studies.

Over time, a one-percent increase in financial globalization will improve Nigeria's commercial banks' ability to extend credit to the private sector by 10 percentage point and above (see Table 5). On an earlier occasion Adegbite and Adetiloye (2013) have shown that financial globalization effect will be marginal in economy. The previous values of credit allocation to the economy have also been shown to affect the present ability of commercial banks to extend credit facility significantly but in a negative way. This indicates the effectiveness of credit management by the commercial banks. It may be interpreted that large loan debt overhang (increased non-performing loan ratio) in banks is a key factor in this negative trend.

More generally, our Error Correction Mechanism lags one term and meets the a priori expectation of being negative. A critical investigation reveals that about 49 per cent of the disturbances in the long run equilibrium trend of credit allocation by commercial banks in Nigeria is corrected annually by the system and that it will take little more than two years (2.04) for the equilibrium trend path of sustained credit allocation to be restored. The Durbin-Watson statistic of 2.01 shows that our variables were not serially correlated. The model also shows that about 50 per cent of fluctuations in credit allocation by the Nigerian commercial banks to the private sector are explained by the independent variables in the model.

In the long run, a one-percent increase in participation in globalization will improve Nigeria's commercial banks' ability to extend credit to the private sector by ten and more percentage points (see Table 6). However, the study shows that continued trade openness to other economies will not benefit commercial banks in the future, nor will Official Development Assistance do in domestic credit allocation. This realization may suggest the workability of structuralist hypothesis of banking operations in Nigeria. The economy, having grown to a steady state of generating positive net income for itself may not necessarily depend on ODA to support development and hence such negative and significant outcome.

Trade openness continued to show a negative significant trend throughout the model. A possible explanation for this may be the product dumping in the country. Nigeria imports different kinds of goods whose production is not financed by the banking system; thereby, this produces such a negative trend throughout the study.

Exchange rate will exert a positive and significant influence on commercial banks credit allocation in Nigeria in the long run. Overtime, Nigeria may become able to fine-tune the exchange rate policies in such a way that a per cent increase in exchange rate will drive foreign revenue to commercial banks for onward lending to the private economy to the tune of 0.1 per cent and couple with falling inflation, thus, accruing more benefits to the economy. The long run relationship also shows that current production of goods and services will not assist commercial banks to make credit allocation to the economy during financial globalization. A percentage increase in current production is sure to reduce commercial banks credit allocation by 0.44 per cent. This may possibly affect the current price of credit in the economy and ultimately make the real price of funds become unattractive both to local and foreign investors by say 4 per cent. Overall, the long run model explains 26 per cent of variations of credit supply by commercial banks to the economy by the independent regressors. The F probability ratio of 0.0001 confirms that our model is a good fit.

Table 6

Long Run Relationship for the Model

Dependent variable: CR*

| Coefficient | Std. Error | t-ratio | p-value | ||||||

| Const | 24.2557*** | 3.9396 | 6.1569 | 0.00001 | |||||

| TOPt | –0.1490** | 0.0651 | –2.2886 | 0.02826 | |||||

| ODAt | –0.0053** | 0.0022 | –2.4326 | 0.02024 | |||||

| EXCRt | 0.0626** | 0.0288 | 2.1722 | 0.03670 | |||||

| INFLt | –0.3790 | 0.2342 | –1.6185 | 0.11454 | |||||

| RGDPt | –0.4377*** | 0.0907 | –4.8276 | 0.00003 | |||||

| Globt | 10.0721*** | 3.3719 | 2.9871 | 0.00512 | |||||

| RRt | –0.3937* | 0.2252 | –1.7483 | 0.08917 | |||||

| Mean dependent var | 16.16791 | S.D. dependent var | 7.180895 | ||||||

| Sum squared resid | 1335.441 | S.E. of regression | 6.177010 | ||||||

| R-squared | 0.383379 | Adjusted R-squared | 0.260055 | ||||||

| F(7, 35) | 6.639658 | P-value(F) | 0.000050 | ||||||

| Log-likelihood | –134.8844 | Akaike criterion | 285.7688 | ||||||

| Schwarz criterion | 299.8584 | Hannan-Quinn | 290.9646 | ||||||

| Rho | 0.578922 | Durbin-Watson | 0.849025 | ||||||

Note: **, *** indicates significance at 5, and 1 per cent respectively.

Source: the author's studies.

5. Conclusions

Globalization has been accepted by most countries of the world as a multiplier of growth and development. After examining the Nigerian case with respect to the performance of commercial banks in credit assistance to the private economy, we found out that a positive effect of globalization in Nigeria is a time-lagged process. One possible reason for this is the dependent nature of the real economy on foreign finished products. Thus, what occupies the country's globalization portfolio are financial proceeds of out-flows rather than inflows. Globalization inflows to Nigeria are merely capital goods whose production finances are made outside the country with Nigerian commercial banks only serving as payment transmission link and hence instead of supporting the real economy positively, the opposite is the case. What happened to Nigeria in the globalization discourse exposes the policy needed for local content development. We recommend improvement on the country's manufacturing and industrial capacity to reverse the trend. Revamping neglected industries in agriculture and energy sectors will boost commercial banks participation in production financing and improve Nigeria's globalization outflows so much that the foreign financial inflows will boost commercial banks performance in Nigeria.

REFERENCES

Adams, S. 2010. Globalization and Economic Growth in Sub Sahara Africa. In Deng, K. (ed.), Globalization – Today, Tomorrow, InTech, DOI: 10.5772/10224. URL: http:// www.intechopen.com/books/globalization--today--tomorrow/globalization-and-economic- growth-in-africa.

Adegbite, E. O., and Adetiloye, K. A. 2013. Financial Globalisation and Domestic Investment in Developing Countries: Evidence from Nigeria. Mediterranean Journal of Social Sciences 6 (4): 213–221.

Ajayi, F. O., and Atanda, A. A. 2012. Globalization and Macroeconomic Stability in Nigeria: An Autoregressive Adjustment Analyses. European Journal of Globalization and Development Research 3 (1): 176–193.

Ajilore, T. 2005. Growth Effects of Capital Accounts Liberalization: Evidence from Vector Error Correction Model in Nigeria. International Journal of Social Sciences 4 (1): 139–151.

Al-Rodhan, N. R. F., Stoudmann, G., and Herd, G. 2006. Proposal for a Globalization Matrix: Quantifying Impacts and Responses. Geneva Centre for Security Policy.

Goyal, K. A. 2006. Impact of Globalization on Developing Countries (With Special Reference to India). International Research Journal of Finance and Economics 5: 1450–2887.

KOF Index of Globalization. URL: http://globalization.kof.ethz.ch/query/. Accessed: 18.06.2015.

Lozane-Vivas, A. A, Pastor, J. T., and Pastor J. M. 2002. An Efficiency Comparison of European Banking Systems Operating Under Different Environmental Conditions. Journal of Productivity Analysis 18: 59–77.

Mamman, A., and Baydoun, N. (n.d.) The Meaning of Globalization: A study in the Nigerian Commercial Banking Sector. Manchester: Institute for Development Policy and Management University of Manchester. URL: http: www.wbiconpro.com/. Accessed: 12.06.2013.

Nwokoma, N. I. 2004. Globalization, Open Regionalism and the ECOWAS Stock Markets. In Ozo Eson, P. I., and Evbuomwan, G. (eds.), Globalization and Africans Economic Development (pp. 483–505). Ibadan: The Nigerian Economic Society.

Ogunleye, E. K. 2008. Financial Globalization and Macroeconomic Performance in Sub-Saharan Africa: Evidence from Nigeria. African Journal of Economic Policy 15 (1): 1–44.

Osamor, I. P., Akinlabi, H., and Osamor, V. C. 2013. An Empirical Analysis of the Impact of Globalisation on Performance of Nigerian Commercial Banks in Post-Consolidation Period. European Journal of Business and Management 5 (5): 38–45.

Ozughalu, U. M., and Ajayi, P. I. 2007. Absolute Poverty and Globalization: A Correlation of Inequity and Inequality. The Nigerian Economic Society Conference on Globalization and Africa's Economic Development (pp. 509–540).

United Nations Conference on Trade and Development. 2003. Management of Capital Flows: Comparative Experiences and Implications for Africa. New York and Geneva.

Uma, K. E., and Obidike, P. C. 2013. An Evaluation of the Contribution of Globalization and Capital Account Liberalization on Economic Development: The case of Nigeria. International Research Journal of Arts and Social Sciences 2 (8): 197–205.

Verter, N., and Osakwe, N. C. 2015. Economic Globalization and Economic Performance Dynamics: Some New Empirical Evidence from Nigeria. Mediterranean Journal of Social Sciences 6 (1): 87–96.

Размещено в разделах