Foreign Trade between Russia and the Balkans in the Context of Global Geostrategic Relations

скачать Автор: Božić-Miljković, I - подписаться на статьи автора

Журнал: Journal of Globalization Studies. Volume 5, Number 2 / November 2014 - подписаться на статьи журнала

Russia has been historically, politically, spiritually, and culturally present at the Balkans for centuries. That is why the relations between Russia and the Balkans have a rich and long tradition. Divisions, wars, economic and political crises since the nineties of the twentieth century have defined, quite a few times, the power relations on the Balkan Peninsula in which Russia has played a prominent place and role. In the geostrategic sense, along with the changes that took place in the late eighties, Russia is increasingly realizing its interests through diverse forms of economic cooperation with most important in economic terms countries and world associations. Among Russia's most important economic partners are almost all Central and East European countries, China, USA, Japan, and European Union. In this context, Russia becomes an increasingly relevant subject of international political and economic relations. Its economic potentials (energy, raw materials, spatial aspect, home market latitude, technological potentials in some economic branches, etc.) make it a very respectable subject of global economy. The last decades of the twentieth century, the cessation of the socialist social structure, the collapse of the USSR and Yugoslavia and the necessity of involvement in the globalization process, have somewhat changed the course of foreign policy both of Russia and of the majority of new Balkan states. Having this in mind, the contemporary relations between the Balkan countries and Russia should be observed in the context of global geostrategic relations in the world, namely those that find their foundations in the process of globalization.

Keywords: foreign trade, Russia, Balkans, globalization.

Introduction

Russia has traditionally and historically played an important role in the Balkans. In recent centuries, one result of the strong ties between Russia and the Balkan nations is a successful overcoming of the crisis of world wars. In recent history, the same relationships have contributed to mitigating the crises of transition in the Balkans. Regardless of the pro-European orientation of the Balkan countries in the period after the Cold War, Russia was and still is a strong political support in the Balkans. However, in economic relations, the opportunities for the future are greater than the results that the economic cooperation currently achieves. It seems that the huge Russian market is too large for the export potential of individual Balkan countries. By contrast, Russia is the most important source of energy for the Balkans, and it also considers the Balkans as a very promising market for the export of various goods and services and the placement of its capital in the form of investment in new and existing economic capacities of the Balkan countries. While both Russia and the Balkans are affected by the global economic downturn, their links have become stronger and are surviving the challenges of a new era.

The focus of this paper is the analysis of foreign trade relations between Russia and the Balkans in the context of the new balance of power in the global economy. The analysis is based on the current state of the economy of Russia and the Balkan countries – with special reference to those Balkan countries which are still in transition. This is followed by an analysis of the situation in terms of foreign trade and opportunities for its improvement, during and after this period of global economic crisis. The paper uses a synthetic and analytical approach and a comparative method of observation of phenomena and processes, using data taken from the available statistical sources of national and international organizations.

The Place of Russia and the Balkans in Contemporary Global Economic Relations

In the last decade of the twentieth century, both Russia and the Balkans faced one of the most difficult periods in their history. The break with the socialist state system, the collapse of both the Soviet Union and Yugoslavia and the necessity to join the globalization process somewhat changed the course of the foreign policy both of Russia itself, as well as of the majority of the newly-created Balkan states. Up to that time, ideologically, culturally and politically related countries had realized that in order to remain in the new global milieu, it is necessary to build an entirely new kind of relationship with the countries in the west and other parts of the world.

A special interest in creating a new strategy for remaining a full-fledged and equal member of the international community is shown by Russia, which sees in this its own chance, as a big country (and a great power), for affecting the political and economic scene in Europe and the world. According to the UN data for 2012, Russia covers an area of 17,075,400 km2, and has 141.2 million inhabitants. That same year, the value of Russian GDP was 1,978.0 billion dollars at current prices and current exchange rates, and was growing at the rate of four per cent in real terms, while inflation was 6.8 per cent, and the unemployment rate was 7.8 per cent.1

The position that Russia has in global economic relations provides for it the role of a reliable political and economic partner in the Balkans. Bulgaria, Romania, Greece, Serbia, Macedonia, Montenegro and other states, due to their shared cultural traditions, are tendency towards good relationship with Russia, though they are, to varying degrees, integrated (or are on the way to being integrated) in the Euro-Atlantic structures. The political influence of Russia in the Balkans (especially in the countries in transition) rests, for the greatest part, upon three pillars. The most important one is the privileged position of Russia as a permanent member of the UN Security Council. Thanks to its right to veto, Moscow can block all the processes controlled by the United Nations in the West Balkans if they contradict Russia's political goals. The second pillar is the historical, cultural, and political connection of Russia with peoples and states in Southeast Europe with an Orthodox tradition. Moscow evidently counts upon such a solidarity relationship to continue as well with those states in the Balkans that are already members of the North Atlantic Treaty Organization (NATO) and the European Union or that have brought about the decision to join these integrations. The third pillar that Moscow relies on in the Western Balkans is the increasing economic impact of Russia on the states of the region. Russia is the main energy provider for the region and it appears more and more as both an investor and a trade partner (Reljić 2009: 6).

Within the European framework, the Balkan region represents its most under-developed area. Judging by almost all economic parameters (their average values for the Balkans), namely, the total GDP, GDP per capita, work force unemployment, volume of export, technological development, and the like, the Balkan region is lagging far behind Western European countries, thus making it a much weaker area of interest for economic cooperation. According to most recent geographical classification, the Balkan countries are: Albania, Bosnia and Herzegovina, Bulgaria, Greece, Croatia, Montenegro, Macedonia, Romania, Slovenia, Serbia, and Turkey. The basic characteristic of these countries is a high degree of political, economic, and cultural heterogeneity. Likewise, their economic development is quite unsteady. The economically more developed Balkan countries include Slovenia, Greece, Croatia, Bulgaria, and Romania (all are members of the European Union), while the remaining countries are undergoing the transition process, at a low level of economic development but with the all-prevailing ambition to join the EU. The Balkan region covers an area of 1,545.3 km2; in 2011, the population numbered 137.8 million people. It has a GDP to the amount of 1,462.7 billion dollars at current prices and current exchange rates. Its average rate of GDP growth is 5.8 per cent. Its average inflation rate is 6.3 per cent in real terms, while unemployment is at 18.4 per cent.2

The base on which Russia and the Balkans build their economic relations is historical, cultural, spiritual, and traditional. Russia has had, historically and politically speaking, a very important role in the Balkans. The fact is that the Balkan peoples managed with great help from Russia to free themselves from the Turks, that the autonomy of Serbia in 1830 had its roots in the Bucharest peace treaty signed by Russia and Turkey in 1812, that independence of Greece largely resulted from the Russian-Turkish war of 1828–1829, that the independence of Bulgaria was likewise a result of the Russian-Turkish war of 1877–1878, and the like.3 Under the present circumstances, regardless of the pro-European orientation of the Balkan countries, Russia remains their important partner and support in global economic relations.4 The economic (especially foreign trade) cooperation between Russia and the Balkans also has its own historical genesis. Regarding the fact that Russia is, economically speaking, closer to the group of developed countries at an ever-increasing rate, and that the Balkans, in terms of the economic development, is considerably lagging behind (in most Balkan countries the transition process is not over yet), one can hardly speak about an intensive mutual economic cooperation. However, it is certainly possible to talk about a cooperation that has good prospects.

Challenges of Sustaining and Developing Economic Relations in the Times of Crisis

The last decade of the twentieth century will be remembered, both in the Russian and the Balkan economies, as a period of transitional crisis. In the nineties, Russia registered a decrease in its GDP for a continual period of eight years, the lowest level being registered in 1998. In 1999, its GDP level came to only 56.1 per cent of the GDP realized ten years earlier in the year preceding the transition. The first signs of the Russian economic recovery became visible in 2000. That year, its GDP growth rate was 10 per cent. In the period from 2000 to 2008, the average annual GDP growth rate was between 4 and 8.5 per cent, but in 2009, under pressure from the global economic crisis, its GDP growth rate fell sharply, and recorded a negative value – 7.8 per cent. Recovery of the Russian economy in the post-crisis years was reflected in stable and positive GDP growth rates, which in 2010 and 2011 amounted explicitly to 4.3 per cent.5 The production drop, inflation, collapse of the banking system, growing social problems, further deepening of social inequalities and uncontrolled or ‘wild’ privatization are its basic problems, dating from the last decade of the twentieth century. Many economic analysts relate the present Russian problems to the USSR (or address them as a legacy of the USSR), its system and economic policy as well as its way of entering the transition process and methods of its realization in 1990 (Rukavišnjikov 2007). They caused the then foreign investors not to show any special interest in investing in the Russian economy. The transition crisis contributed to the crystallization of the Russian attitude that it had to change its strategic orientation in its economic relations with foreign countries. Thus, it opted for economic openness to the world at large as opposed to only the former republics of the USSR and members of the Commonwealth of Independent States. The changes that have been made in the last few years in this direction in Russia have allowed for a greater influx (and presence) of foreign companies in its economy and a greater influx of foreign investments, as well as increased export of Russian capital and a growth in sales of Russian products on the world market.

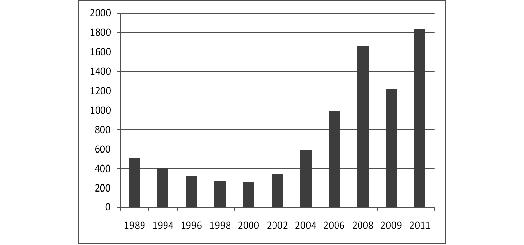

Though Russia can be said to have overcome its transitional crisis and established its solid position in new global economic relations, the macroeconomic indicators (especially those related to GNP) reveal its slow economic development. Namely, the Russian economy needed fifteen years to achieve the GNP value of the pre-transition year of 1989.

Fig. 1. Russian GNP fluctuations in the period from 1989 to 2011 (US Dollars at current prices and current exchange rates in billion)

Source: URL: http://unctadstat.unctad.org/TableViewer/tableView.

On the basis of the data shown in Fig. 1, one can say that from 2004 onwards, the Russian economy has been undergoing a more intensive and stable development. Some American experts had even predicted that the year of 2010 would be that of the flourishing of the Russian economy. And they were right. These optimistic prognoses proceeded from the experts' assumption that raw materials, now as before, are the backbone of the Russian economy's development. However, a great financial (and then economic) crisis as well as a sudden fall in the oil price in 2008 have both shown that even the most realistic prognoses at first sight should be taken critically into consideration. The forecasts (especially those referring to the demand for energy resources in the world market) cannot be instruments for planning economic development. Under the new global conditions, the high degree of dependence of the Russian economy on the export of raw materials is a problem rather than a pillar of its economic development. This is further supported by a decline in the GDP of over 20 per cent (see Fig. 1) in 2009 in comparison with 2008. This decline was caused by the world economic crisis, as well as a drop in the value of energy resources in the world market. In order to prevent any negative effects caused by fluctuations in the prices of raw materials and energy resources in the world market, the main task of today's Russia is the modernization of its economy and its overall social system, which should be carried out in line with new technologies and innovations. Along with looking for new possibilities for the exploitation and processing of energy resources, what should also be supported is the development of those branches of industry that are focused on manufacturing sophisticated industrial products that would be competitive in the world market.

Following on from the above-described heterogeneous structure of the Balkan region, it should also be mentioned that the region comprises countries that have not undergone the process of transition (Greece and Turkey), countries that have successfully completed it (Slovenia, Croatia, Romania, and Bulgaria), and the rest of the Balkan countries in which the transition process is still going on and its completion time is still uncertain.6 More than two decades have passed since the beginning of transition in the Balkans, with slight time differences due to different dates when particular countries took on prescribed reforms.

Table 1

Fluctuations of the Balkan countries' GDP in the period from 1989 to 2011 (US Dollars at current prices and current exchange rates in billion $)

|

| 1989 | 1995 | 2000 | 2004 | 2008 | 2009 | 2011 |

| Albania | 3.0 | 2.5 | 3.6 | 7.3 | 13.1 | 12.0 | 12.9 |

| Bosnia and Herzegovina | – | 2.0 | 5.5 | 10.0 | 18.5 | 17.0 | 18.3 |

| Bulgaria | 22.0 | 13.4 | 12.9 | 25.3 | 51.8 | 48.6 | 53.5 |

| Croatia | – | 22.1 | 21.5 | 41.0 | 69.3 | 63.4 | 63.9 |

| Greece | 76.2 | 131.7 | 127.1 | 230.0 | 341.2 | 321.8 | 298.4 |

| Macedonia | – | 4.5 | 3.6 | 5.5 | 9.8 | 9.3 | 10.2 |

| Romania | 56.8 | 35.7 | 37.3 | 75.8 | 204.3 | 164.3 | 186.6 |

| Serbia* | – | 24.1 | 11.4 | 28.8 | 53.4 | 45.6 | 50.8 |

| Montenegro | – | – | – | – | 4.5 | 4.1 | 4.6 |

| Slovenia | – | 20.9 | 20.0 | 33.8 | 54.6 | 49.0 | 50.0 |

| Turkey | 144.0 | 227.6 | 266.7 | 392.2 | 730.3 | 614.6 | 778.5 |

* Data from 1995 to 2008 included Montenegro.

Source: UNCTAD, Handbook of Statistics. URL: http://unctadstat.unctad.org/Table Viewer/table View.aspx.

The period is surely sufficiently long enough to allow for making some estimates of what has taken place and the results of the applied reforms. The analysis of the GDP obtained in the observed period shows that its value is greatest for the EU member countries and for Turkey, while the group of transition countries (of the former SFR of Yugoslavia without Slovenia, with Albania) achieved considerably lower GDP values and, in terms of percentage, lower growth rates compared to the more developed neighbors in the region. According to UNCTAD data, the GDP value of the former SFR of Yugoslavia, in 1989 (as the pre-transition year) amounted to $ 81.8 billion. The data presented here illustrate the fact that none of the countries that became independent in this twenty-year long period ever reached that GDP value. The only exceptions are Croatia, Serbia and Slovenia that managed, in 2011, to realize respectively 78 per cent, 62 per cent and 60 per cent of the pre-transition GDP.

It can be said that in the Balkan countries in transition, the transitional crisis is still going on. It represents an obstacle to their better positioning in global economic relations. On the basis of the data from Table 2, it is evident that the world economic crisis has not passed the Balkans by. Namely, all the countries, in 2009, recorded a decline in their GDP in comparison with 2008. The GDP decline is a consequence of the decreased inflow of direct foreign investment, as well as a general decline in production that has, in the last few years in the Balkans (especially in the transition countries), taken on enormous proportions.

The experience so far in the relations between Russia and the Balkans speaks about the fact that Russia has a considerable political, yet even greater economic influence that proves to be resistant to any critical conditions. Russia is the main energy provider for the whole of Southeastern Europe including the Balkans. In addition, its presence is evident as well as its participation in the privatization process, a process that has also been carried out in Russia within the transition process. The 1990s both in Russia and in the Balkans were committed to adjusting to the newly-created situation and the challenges of the new global world order. After that decade, which was marked, in both regions, by occasional political instabilities and a chaotic transition from central planning to a market economy, new possibilities were created in the early new century for a wider economic presence of Russia in the Balkans, and for further advancement of their economic relations. For instance, in the late nineties in Romania and Bulgaria, the first petrol stations belonging to the Russian oil giant Lukoil were opened, while in 2005 the same investment reached Serbia as well. This was the beginning of the Russian investment expansion in the Balkan region. Two years later, the value of the Lukoil investment in the Southeastern European region, including the Balkans, amounted to one and a half billion American dollars. Annual deliveries of natural gas to the Southeastern European region have reached seven billion cubic meters, which is approximately half of the quantity Russia delivers to the EU.7 After the financial strengthening of Russia in the first decade of the twenty-first century, at a time of high raw material prices in international trade, Moscow did not only become a desired economic partner in Balkan energy, but also, in the meantime, numerous Russian companies started to invest into the machine and motor vehicle industry, the production of non-ferrous metals, tourism, banking and other economic domains in the region. The greatest investments, in terms of volume and value, are those in Montenegro. It can be said that its economic dependence on the Russian partners in the period before the great world economic crisis reached a critical level. Russian entrepreneurs have invested two billion American dollars into this country of about 650,000 people, while approximately 30,000 Russian citizens have bought land and housing in this small Adriatic country. Half of Montenegro's income from exports was made, until the breakout of the world economic crisis, by the Aluminum Company of Podgorica or KAP. This factory was on the verge of being liquidated in early 2009. It is in majority ownership by RUSAL, the greatest world aluminum producer. The closing of KAP would mean a serious blow to the overall national economy of this small country (European Parliament 2007). Not a single Balkan state has established such close relations with Russian economic partners as Montenegro has. Russian companies are, however, powerfully present throughout the Balkans. They are most present in the domain of petrochemistry. Thus, for instance, Zarubežneft owns the most important companies in the petrochemical industry in the Republic of Srpska and the big Russian oil company Lukoil is the leader in raw oil and fuel provision, while Gazprom dominates the Balkan market for natural gas.

Despite both Russia and the Balkans being struck by the world economic crisis, Russia, due to its strong position in energy, has a considerable advantage, enabling it to preserve its image as an important economic partner for a long period of time. Thus, it has been able to strengthen its political position in the Balkans by demonstrating the fact that, in terms of new global relations, it is a more reliable partner than the European Union.8

Foreign Trade Relations between Russia and the Balkans

The presence in the Balkans is one of the strategic economic interests of Russia. Yet, the facts make it obvious that Russia is still a long way away from having a long-term Balkan strategy, namely, the one that would imply its greater political and economic presence there. Still, regardless of this, in the last decade there has been a shift in this direction in relations between Russia and the Balkan countries. An evidence of this is an increasing volume of foreign trade between Russia and individual Balkan countries. As can be seen from Table 2, all the Balkan countries register a rising trend in their foreign trade with Russia, regardless of the fact that some of them have meanwhile become members of the EU or have been working intensively on the process of the EU integration.

Table 2

Foreign Trade Exchange between the Balkan Countries and Russia in the period from 2001 to 2011 (nominal US dollars in billion)

| Export to Russia | ||||||

| 2001 | 2003 | 2005 | 2007 | 2009 | 2011 | |

| Albania | 0.0 | 0.0 | 0.1 | 0.0 | 0.0 | 0.1 |

| Bosnia and Herzegovina | – | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 |

| Bulgaria | 0.1 | 0.1 | 0.1 | 0.4 | 0.4 | 0.7 |

| Croatia | 0.1 | 0.1 | 0.1 | 0.2 | 0.1 | 0.3 |

| Greece | 0.3 | 0.3 | 0.4 | 0.5 | 0.3 | 0.5 |

| Macedonia | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 |

| Romania | 0.1 | 0.1 | 0.2 | 0.6 | 0.7 | 1.4 |

| Slovenia | 0.3 | 0.4 | 0.6 | 0.9 | 0.7 | 1.0 |

| Serbia* | 0.1 | 0.1 | 0.2 | 0.4 | 0.3 | 0.8 |

| Montenegro | – | – | – | 0.0 | 0.0 | 0.0 |

| Turkey | 0.9 | 1.4 | 2.4 | 4.7 | 3.2 | 6.0 |

| Import from Russia | ||||||

| 2001 | 2003 | 2005 | 2007 | 2009 | 2011 | |

| Albania | 0.01 | 0.05 | 0.1 | 0.2 | 0.1 | 0.1 |

| Bosnia and Herzegovina | – | 0.03 | 0.2 | 0.2 | 0.6 | 1.2 |

| Bulgaria | 1.5 | 1.4 | 0.4 | 5.1 | 3.6 | 5.7 |

| Croatia | 0.6 | 0.7 | 1.7 | 2.6 | 2.0 | 1.6 |

| Greece | 1.6 | 2.7 | 4.2 | 4.3 | 3.4 | 5.8 |

| Macedonia | 0.1 | 0.2 | 0.4 | 0.6 | 0.5 | 0.7 |

| Romania | 1.2 | 2.0 | 3.3 | 4.4 | 2.1 | 2.9 |

| Slovenia | 0.3 | 0.4 | 0.4 | 0.7 | 0.3 | 0.6 |

| Serbia* | 0.7 | 1.4 | 1.7 | 2.6 | 2.0 | 2.6 |

| Montenegro | – | – | – | 0.04 | 0.03 | 0.01 |

| Turkey | 3.4 | 5.4 | 12.9 | 23.5 | 19.7 | 23.9 |

* Data from 2001 to 2005 refer to Serbia and Montenegro.

Source: URL: http://comtrade.un.org/db/dqQuickQuery.aspx

These data lead us to conclude that the most important foreign trade partners of Russia among the Balkan countries are Turkey and the EU member countries (Greece, Romania, Bulgaria, and Slovenia). It can also be noted that during the whole observed period, Turkey has been in the first place in terms of its exports to the Russian Federation which, in 2011, amounted to as much as six billion dollars (more than all the other Balkan countries put together). Second on the list is Romania with 1.4 billion dollars, followed by Slovenia, Serbia, and Bulgaria. The situation is similar concerning imports, where Turkey indubitably holds the first position, followed by Greece, Bulgaria, Romania, and Serbia. Albania, Macedonia, and Bosnia and Herzegovina have modest participation in foreign trade with Russia.

Among the Balkan countries in transition, Serbia is Russia's most important economic partner. Regardless of the negative impact of the world economic crisis, 2010 was characterized by a renewal and increase in the volume of inter-trade. According to the treaty on cooperation in oil and gas domains, there is continued cooperation in the realization of large-scale energy projects, including the building of the Serbian part of the South Stream gas pipeline whose trajectory starts from southern Russia via the bottom of the Black Sea and via Southeastern Europe to Italy.9 In addition, Russian projects in Serbia also include the arrangement and launching of the underground storage ‘Banatski Dvor’ and the modernization of production capacity in the oil industry of Serbia. There are also plans in the domain of development of traffic and infrastructure. According to the Serbian Chamber of Commerce data, the volume of Russian investment in the Serbian economy in the period from 2003 to 2011 amounts to about 1.6 billion dollars in current prices (Serbian Chamber of Commerce 2013). The fact is that on the part of Russia there are ambitions and plans for economic (primarily foreign trade) cooperation not only with Serbia but with the whole West Balkan region. The political stability of the sub-region will be a decisive factor for the realization of the intended cooperation.

Balkan countries, on the whole, import, for the largest part, raw oil, oil derivatives, natural gas and machines and equipment from Russia, while what dominates Russia's imports are products from the processing industries and food. The import structure clearly points to the high energy dependence of the Balkan countries on Russia. Europe is a continent with scarce energy resources and according to the estimates made by distinguished energy consulting houses, in ten years Europe will buy 670 billion cubic meters of gas. Europe imports the largest quantities of energy resources from Russia (32.4 per cent), Norway (16.8 per cent), Saudi Arabia (10.5 per cent), Libya, Kazakhstan, Algeria, Iran, Nigeria, and Syria (others 40 per cent). This import structure is different in the case of the Balkan countries. They are, in their import, largely Russia-oriented. Some of them are completely import-dependent while with others, this import-dependence is present to a high extent. For instance, countries like Bosnia and Herzegovina, Bulgaria, Macedonia, Greece, and Serbia are completely dependent on the import of Russian gas while the share of Russian gas in the overall import to Turkey is 78 per cent, Croatia 65 per cent, Romania 63 per cent, Slovenia 51 per cent and Albania 51 per cent (Rapaić 2009: 527). The absorption potential of the Russian market is not sufficiently used by the Balkan countries for promotion of their products. The enormous Russian market demands huge and continuous deliveries, and not a single Balkan country can meet these requirements on its own (with the exception of Turkey). The solution can be found in the linkage and cooperation of the Balkan countries when it comes to common production and export to Russia and other huge and distant markets. A concrete shift towards common cooperation and export affairs is done through the CEFTA agreement which includes all the countries of the West Balkans and Moldova. The other Balkan countries that are members of the EU organize their exports within this integration. The great absorption capacity of the Russian market allows for exports from Balkan countries to this market to be much larger than it is currently realized. An increase in exports would help the foreign trade between Russia and the Balkans become more balanced in view of the fact that the enormous import of oil and gas from Russia is causing the Balkan countries to have a deficit in their foreign trade with Russia.

Possibilities for Advancing Foreign Trade and Economic Relations between Russia and the Balkans

The role of generators of foreign trade between Russia and Balkan countries has been assigned, in most recent years, to the Russian companies that have invested their capital more and more into organizing production and other economic activities in the given countries. Almost all the Balkan countries have witnessed an accelerated growth of investment on the part of the Russian companies and Russian capital (Radak 2007: 14). The forms of these investments are most often the purchases of companies in the process of privatization (in the transition countries) and, less often, greenfield investments. Structurally speaking, the largest part of these investments has been in the sector of processing and distributing oil and gas (investments of the companies Lukoil, Gazprom, Gazprom Neft and others in Bulgaria, Rumania, Serbia, Republic of Srpska, etc.), then in base metal production (investments into ironworks in Croatia and Romania, production of aluminum in Romania and Montenegro and the like) as well as in the manufacturing sector (manufacturing of machinery, building materials, drug production, food industry, etc.) and investment in the tourist capacities in Turkey, Bulgaria, Montenegro, and Albania. It is interesting that among the Balkan countries, Slovenia is one of the largest investors in the Russian economy and the only country with a surplus in trade with Russia. It has invested in the drug manufacturing, as well as in telecommunication equipment and the manufacture of dyes and lacquers and of baby food (in total, over 120 million nominal dollars in the period from 2002 to 2009). Likewise, an important part of the Slovenian manufacturing capital invested into Serbia has directed its production towards exports, and this to the Russian market. One can explain this by the benefits that Serbia has in its trade with Russia that were set up by a special agreement on the liberalization of their mutual trade, dating from 2000.10 On the other hand, the presence of Balkan companies at the Russian market, in terms of foreign investments, is negligible. Several of them from Greece, Turkey and Slovenia, in a certain sense, represent harbingers of greater future investments.

It has already been stated that the export of oil and gas is at the core of Russia's foreign relations with Balkan countries. Balkan countries import Russian oil and gas for their needs, whilst also providing a transit route for transporting energy resources to Western Europe. For this purpose, preparations are currently underway for building oil and gas pipelines, one of which is the South Stream which should secure a good supply of these energy resources not only to Balkan countries, but also to some EU member countries outside the Balkans. However, in terms of future prospects, the trade between Balkan countries and Russia should not be reduced only to the energy sector. On the contrary, it should comprise numerous other sectors of production of goods as well as services.11 From a long-term perspective, the energy sector, in this respect, can represent a link as well as a factor in the development of other kinds of relationships in other domains of trade.

Conclusion

These good neighborly relations and cooperation of the Balkan countries with Russia have a very long tradition, and thus they have been sustained and can be further developed on a stable basis. They have also successfully resisted the challenges of new global relations. The fact is that in the post-cold war period, all the Balkan countries show a pro-European orientation and make considerable political and economic effort for a faster integration into the European Union. It is well known that foreign trade, that is, the interest leading to liberal trade relations among countries is a safe way and initial triggering-off for every other form of linkage and cooperation. For this reason the Balkan region is developing its most intensive trade relations with the European Union countries, hoping that in this way it will become a member in the near future. However, regardless of these pro-European ambitions, in the politics of the regional orientation of their foreign trade in the future, the Balkan countries should pay special attention to the development of their trade relations with Russia for many reasons such as:

– firstly, the Russian market is large and it has great absorption power; moreover, it is a market in expansion.

– secondly, there are traditionally good economic and other relations between the majority of the Balkan countries and Russia.

– thirdly, there is a certain degree of compatibility between the Russian and the majority of the Balkan countries' industries that has its roots in the history of their interrelations, and which may represent a positive factor in the development of their trade relations and their inter-trade in the future.

– fourthly, the Balkan countries depend, to a high extent, on Russian deliveries of oil and gas; and,

– fifthly, the presence of Russian capital and companies is considerably felt in the economies of the Balkan countries, and in the future their even greater presence and even more important activities are to be expected.

What is important for the foreign trade (especially export) of the Balkan countries with Russia is the existence of competition in the Russian market. Namely, Russia is also in the process of globalization and regionalization, carrying out a strategy of opening up to the world and liberalizing its foreign trade, which enables the presence of commodities from all over the world in its market. Another thing that should be taken into account is the volume of the commodity offer in its market and the ability to sustain deliveries. The vast Russian market requires large deliveries and their continuity. The size of these deliveries very often surpasses the capacity of a single producer or even a country. The problem could be overcome by integrating the same products from different countries, with the aim of commonly manufacturing products designed for the Russian market. The condition for this is that the process of regionalization in the Balkans should meaningfully comprise, among other things, cooperation among the countries in the region for the sake of manufacturing products designed for other markets. In that sense, very attractive branches for export to the Russian market can be food industry, chemical industry, construction sector with accompanying industry, pharmaceuticals, metal processing and textile industries, some sectors of wood processing industry and other branches of industry.

NOTES

1 Data on area, population and macroeconomic indicators: URL: http://unctadstat.unctad.org/ TableViewer/tableView.aspx?ReportId. Accessed 11 Sept. 2013.

2 Calculated on the basis of the data taken from URL: http://unctadstat.unctad.org/Table Viewer/ tableView.aspx?ReportId. Accessed 11 Sept. 2013.

3 For more historical details see: Terzić Slavko, historian and Balkanologist, Radio Free Europe, interview: ‘Is Russia Coming Back to the Balkans?’ (Da li se Rusija vraća na Balkan?), available May, 6, 2010. More details can be found at URL: http://www.slobodnaevropa.org/content/Transcript/703309. html). Accessed 18 Jan. 2011.

4 Russia is one of the few countries that have not so far acknowledged the one-sided declared independence of Kosovo and Metohija (although it has recognized in the same way the declared independence of its own provinces of Ossetia and Abkhazia).

5 Source of data: EBRD, Transition Report 1999: 27; and World Bank: Development Indicators 2006: 195; and URL: http://databank.worldbank.org/ddp/html-jsp/QuickViewReport.jsp. Accessed 20 Apr., 2013.

6 Those countries are: Albania, Bosnia and Herzegovina, Serbia, Montenegro, and Macedonia.

7 President of Russia, Speech at the Balkan Energy Cooperation Summit, Zagreb, June, 24, 2007, Source: URL: www.kremlin.ru/eng/text/speeches/2007/06/24/1214_type82912type82914_135740.html. Accessed 30 Jun. 2007.

8 When, in 2008, due to the world economic crisis the Italian car manufacturer Fiat gave up its investment (worth 700 million Euros) in the Serbian company Zastava, the former Russian ambassador Konuzin, on his visit to Kragujevac, mentioned that Russia always keeps its promises when it comes to business plans. Serbia is, as he said, the only country outside the Community of Independent States that possesses an inclusive agreement on free trade with Russia. This agreement would, after Serbia joins the EU, become invalid. Source: ‘Ambassador Konuzin: Russia will Realize its Agreed Investments’ (‘Ambasador Konuzin: Rusija će realizovati dogovorene investicije’), Beta News Agency, April, 16, 2009.

9 The basic agreement of the Russian company Gazprom with the national gas companies of Serbia, Bulgaria, Italy, and Greece that are on the gas pipeline trajectory was signed on May 15, 2009 in Sochi. On 20 February 2013, the Serbian parliament adopted a law on the ‘South stream’ which will accelerate the expropriation of land and prepare the ground for the construction of the gas pipeline across Serbia. It is expected that the construction of the pipeline will begin in January 2014. For more details visit the website of the Serbian Government: http://www.srbija.gov.rs/vesti/vest.php?id= 184331. Accessed Febr. 2013.

10 More details in the Website Gospodarska zbornica Slovenije: www.gzs.sl. Accessed 25 Feb. 2013.

11 In 2011, for instance, the overall trade import of Russia was $ 87.9 billion; of this only 350 million was from Serbia. The main export products of Serbia to Russia in the same year were: flooring and wall papers (11.6 per cent), paper, cardboard (7.5 per cent), medicaments (7.03 per cent), side-cars and semi-sidecars (6.7 per cent), devices and laboratory equipment (6.6 per cent), floor tiles (5.7 per cent), refined copper pipes (2.9 per cent), fruit (2.7 per cent), conductors (2 per cent), hoists (1.8 per cent), corn (1.7 per cent) and the like. Source: Serbian Chamber of Commerce. 2013. URL: http://www. pks.rs/MSaradnja.aspx?id=50. Accessed 25 Apr. 2013.

REFERENCES

EBRD. 1999. Transition Report. London: European Bank for Reconstruction and Development.

European Parliament. 2007. The Russian Economic Penetration in Montenegro. Briefing Paper. Brussels: European Parliament.

Konuzin, A. 2009. Russia will Realize Its Agreed Investments. Interview Beta News Agency. April 16.

Putin, V. 2007. President of Russia. Speech at the ‘Balkan Energy Cooperation Summit’. Zagreb. June 24. URL: www.kremlin.ru/eng/text/speeches/2007/06/24/1214_type82912 type82914_135740.html. Accessed 30 Jun. 2007.

Radak, I. 2007. The Balkans – A Stopover for Russian Capital. Danas, December 10: 14.

Rapaić, S. 2009. Energy Resources Market in the European Union and Serbian Interests. International Problems 61(4): 515–535.

Reljić, D. 2009. Russlands Rückkehr auf den Westlichen Balkan. SWP-Studien. Stiftung Wissenschaft und Politik Deutsches Institut für Internationale Politik und Sicherheit. July, 2009. Berlin.

Rukavišnjikov, V. 2007. Russia's Power and Competitiveness. International Problems 59(4): 487–512.

Serbian Chamber of Commerce. 2013. International Cooperations. Belgrade. URL: http://www.pks.rs/MSaradnja.aspx?id=51&p=1&pp=0&. Accessed 25 Apr. 2013.

Serbian Government. 2013. Building of the South Stream Pipeline to Higher Energy Efficiency. Belgrade: Vlada Republike Srbije. URL: http://www.srbija.gov.rs/vesti/vest. php?id=184331. Accessed 25 Febr. 2013.

UNCTAD. 2012. Handbook of Statistics. Geneva. URL: http://unctadstat.unctad.org/ TableViewer/tableView.aspx?ReportId. Accessed 11 Sept. 2013.

United Nations Commodity Trade Statistics Database. 2012. International Trade Statistics Yearbook. New York: United Nations. URL: http://comtrade.un.org/db/dqQuickQuery. aspx. Accessed 20 Apr. 2013.

WORLD BANK. 2006. World Development Indicators. Washington.

Размещено в разделах